When Winter Storage Turns Into an Insurance Fight

You parked your vehicle for the winter, kept insurance in place, and assumed you were protected. Then something happened—a theft, a fire, storm damage, vandalism, or another loss—and now your insurance company is questioning your claim. While insurers are entitled to investigate claims, that doesn't mean a denial is automatically correct. Understanding how storage coverage works and what evidence insurers typically require can improve your chances of getting a valid claim paid.

Luis Molinero, Shutterstock.com

Luis Molinero, Shutterstock.com

Understand Why The Claim Is Being Questioned

Insurance companies often scrutinize claims involving stored vehicles because the circumstances can be difficult to verify. They may want proof that the vehicle was actually in storage, confirmation that the damage occurred during the policy period, or evidence that the loss falls under a covered peril rather than an excluded event.

Review Your Policy Before Arguing Your Case

The strongest position starts with your insurance contract. Read the declarations page, endorsements, and exclusions carefully. Many seasonal storage arrangements involve reducing coverage rather than canceling it entirely, and the exact protection depends on the wording of the policy.

Confirm You Kept Comprehensive Coverage

For stored vehicles, comprehensive coverage is usually the key protection. It commonly covers theft, fire, vandalism, weather-related damage, falling objects, and certain other non-collision losses. If comprehensive coverage remained active during storage, that is often the foundation of a valid claim.

Ildar Sagdejev (Specious), Wikimedia Commons

Ildar Sagdejev (Specious), Wikimedia Commons

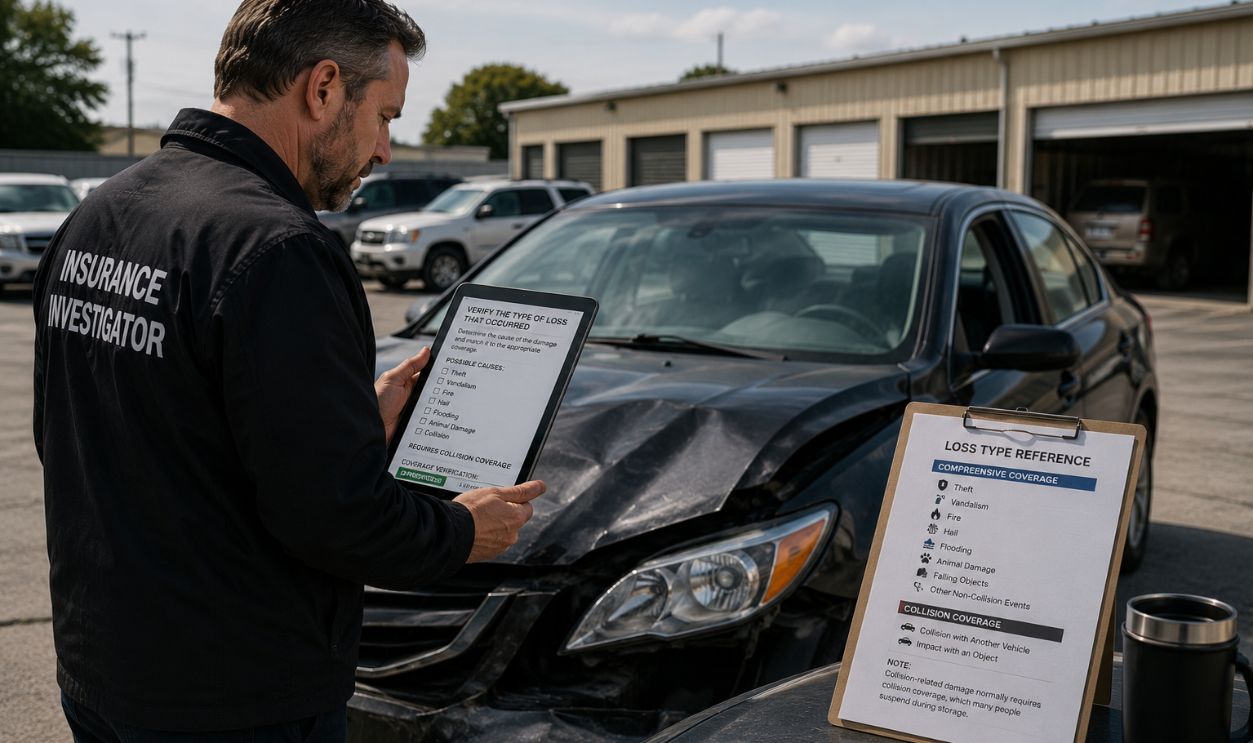

Verify The Type Of Loss That Occurred

Not every loss is covered simply because a vehicle is insured. Comprehensive coverage generally applies to theft, vandalism, fire, hail, flooding, animal damage, and similar risks. Collision-related damage normally requires collision coverage, which many people suspend during storage.

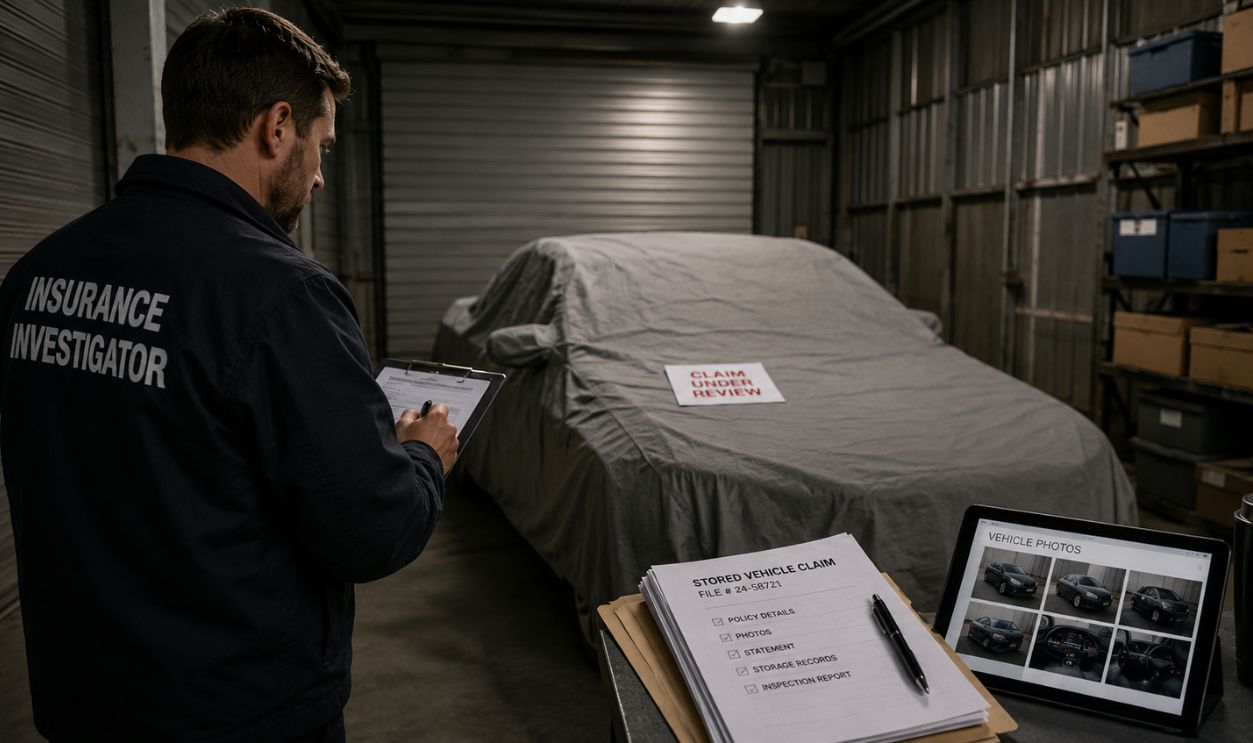

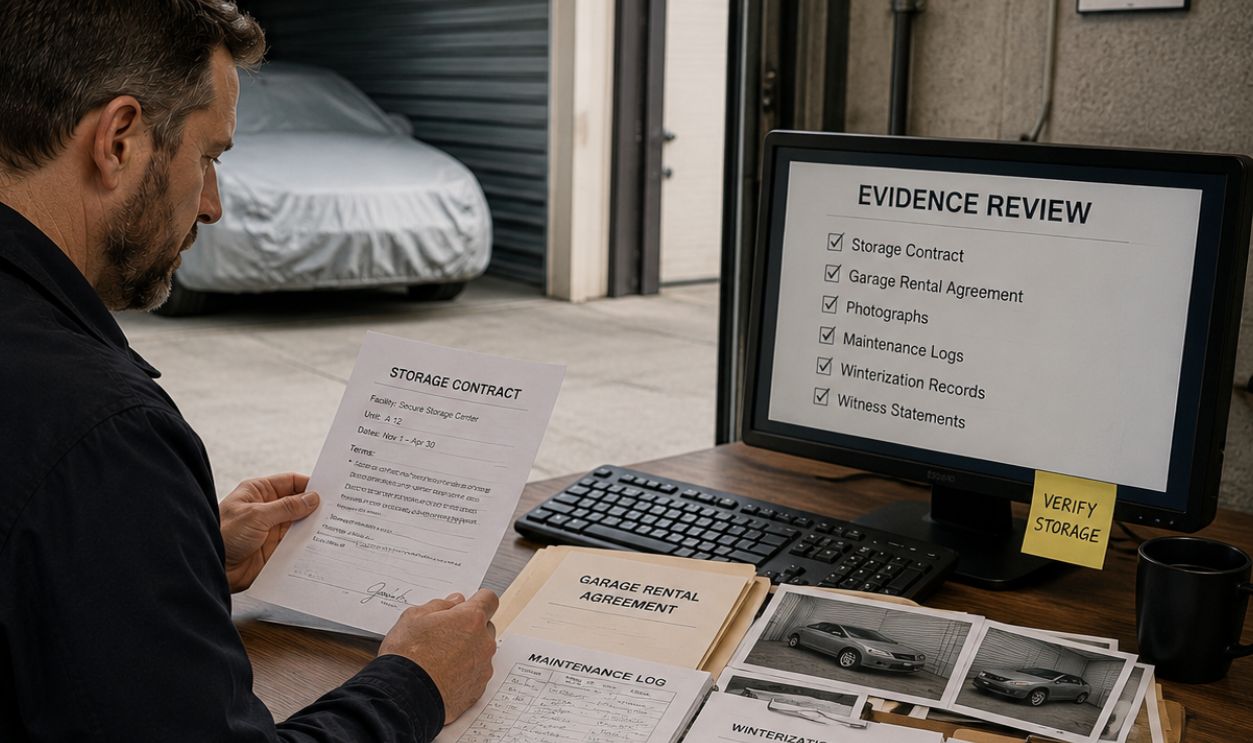

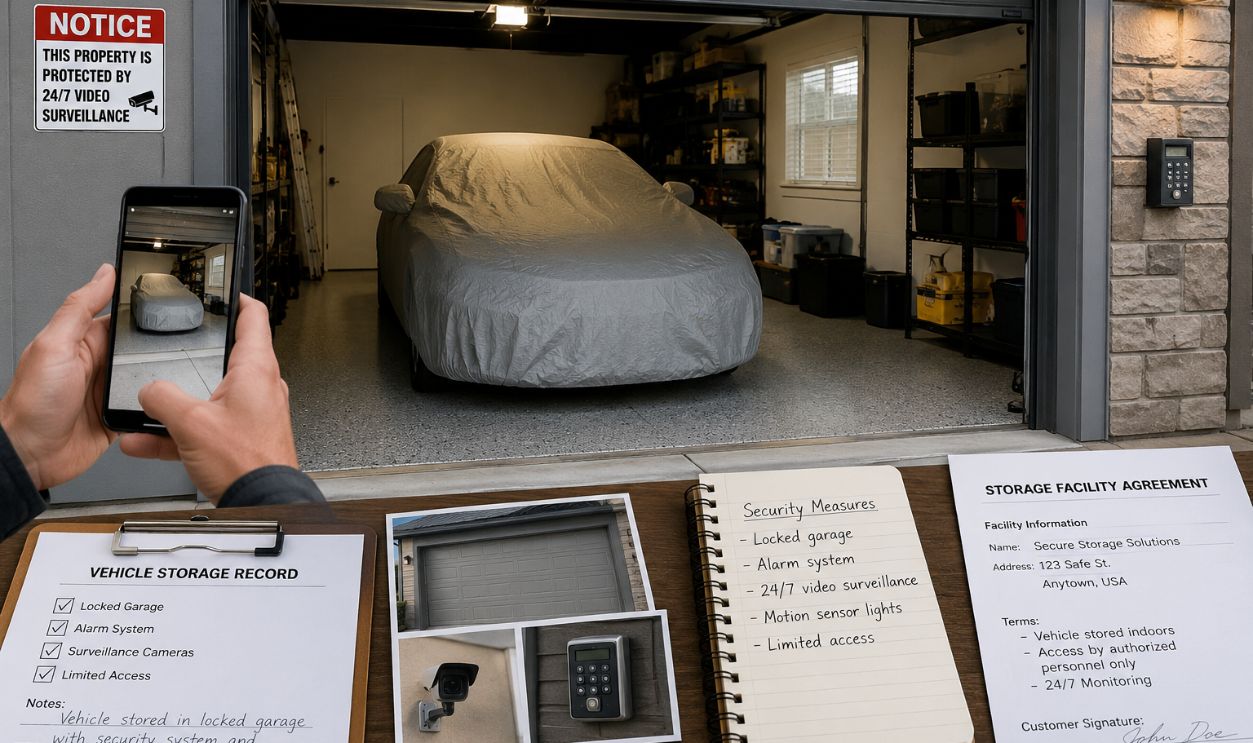

Gather Proof The Vehicle Was Actually Stored

Insurers may ask for evidence showing the vehicle was not being driven. Storage contracts, garage rental agreements, photographs, maintenance logs, winterization records, or witness statements can help demonstrate that the vehicle remained where you said it was.

Show That Premiums Were Paid

Coverage only exists if the policy remained active. Keep copies of payment confirmations, billing records, policy renewals, and any communications showing the insurer accepted premiums during the storage period.

Document The Vehicle’s Condition Before Storage

Photos taken before winter storage can become valuable evidence. They help establish that the damage did not exist beforehand and can counter arguments that the loss resulted from pre-existing issues.

Keep Records Of How The Vehicle Was Protected

Many insurers expect policyholders to take reasonable precautions. If the vehicle was stored in a locked garage, monitored facility, or secured location, provide documentation and photographs demonstrating those security measures.

Report Theft Or Vandalism Immediately

If the claim involves theft or vandalism, reports from authorities are often essential. Delays in reporting can raise questions about credibility and make it harder to establish when the loss occurred.

Obtain Independent Repair Estimates

An insurer's estimate is not necessarily the final word. Independent repair shops can provide assessments of the damage and may identify causes or repair costs that differ from the insurer's conclusions.

Ask For The Exact Reason In Writing

If the insurer questions or denies coverage, request a written explanation. Insurers generally provide specific reasons tied to policy language, and understanding the precise basis for the dispute is critical before responding.

Compare The Denial To The Policy Language

Many disputes arise because consumers rely on verbal explanations instead of the contract itself. Compare the insurer's stated reason with the actual policy wording to determine whether the denial is supported by the language of the policy.

Provide Additional Evidence Promptly

Claims investigations often hinge on documentation. If the insurer requests photographs, receipts, reports, storage records, or witness statements, provide them quickly and keep copies of everything submitted.

Correct Factual Errors Immediately

Insurance investigations sometimes contain mistakes. The adjuster may misunderstand where the vehicle was stored, when the damage occurred, or what coverage existed. Responding with clear documentation can resolve some disputes without escalation.

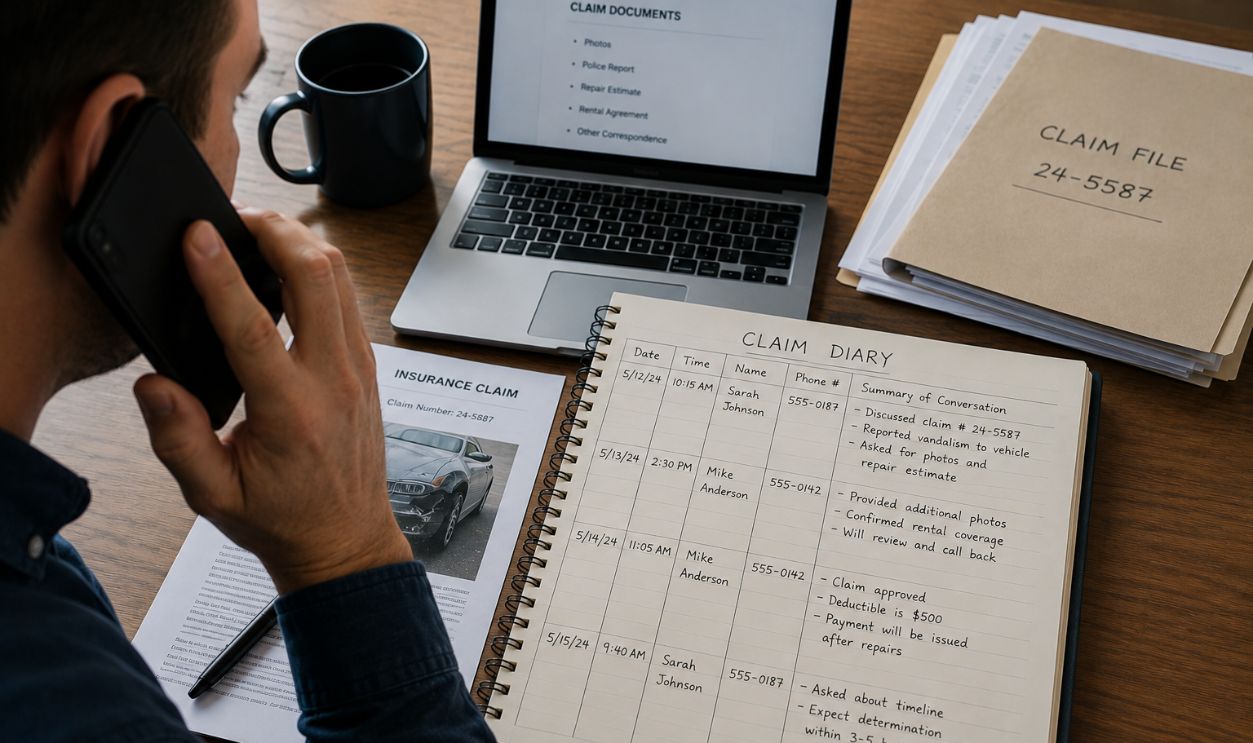

Keep Detailed Notes Of Every Conversation

Create a claim diary. Record dates, names, phone numbers, and summaries of conversations. If disagreements arise later, contemporaneous notes can help establish what information was provided and when.

Request A Supervisor Review

If discussions with the adjuster stall, ask for a supervisor or claims manager to review the file. A second review sometimes identifies errors, overlooked evidence, or misunderstandings that can be corrected internally.

Use The Insurer’s Formal Complaint Process

Most insurers maintain internal complaint procedures. Following those processes demonstrates that you attempted to resolve the issue professionally and creates a documented record of the dispute.

Contact The Appropriate Insurance Regulator

If you believe the insurer is acting improperly, regulatory agencies may be able to explain consumer rights and complaint options. Regulators generally do not decide claim payouts, but they can help ensure proper procedures are followed.

Consider Professional Assistance

When substantial money is involved, consulting an insurance lawyer or licensed claims professional may be worthwhile. Coverage disputes often turn on technical policy language that experienced professionals understand better than most consumers.

Focus On Evidence Rather Than Emotion

The most successful claim disputes are usually evidence-driven. Insurers make decisions based on policy language, documentation, expert opinions, and factual records. The more objective proof you provide, the stronger your position becomes.

Persistence Often Matters

A questioned claim is not necessarily a lost claim. Many disputes are resolved after additional documentation is provided or after a higher-level review occurs. Staying organized, responding promptly, and grounding your arguments in the policy's actual wording gives you the best chance of obtaining coverage if the claim is legitimately covered.

You May Also Like:

My extended warranty won’t cover a known defect. Isn’t that what extended warranties are for?