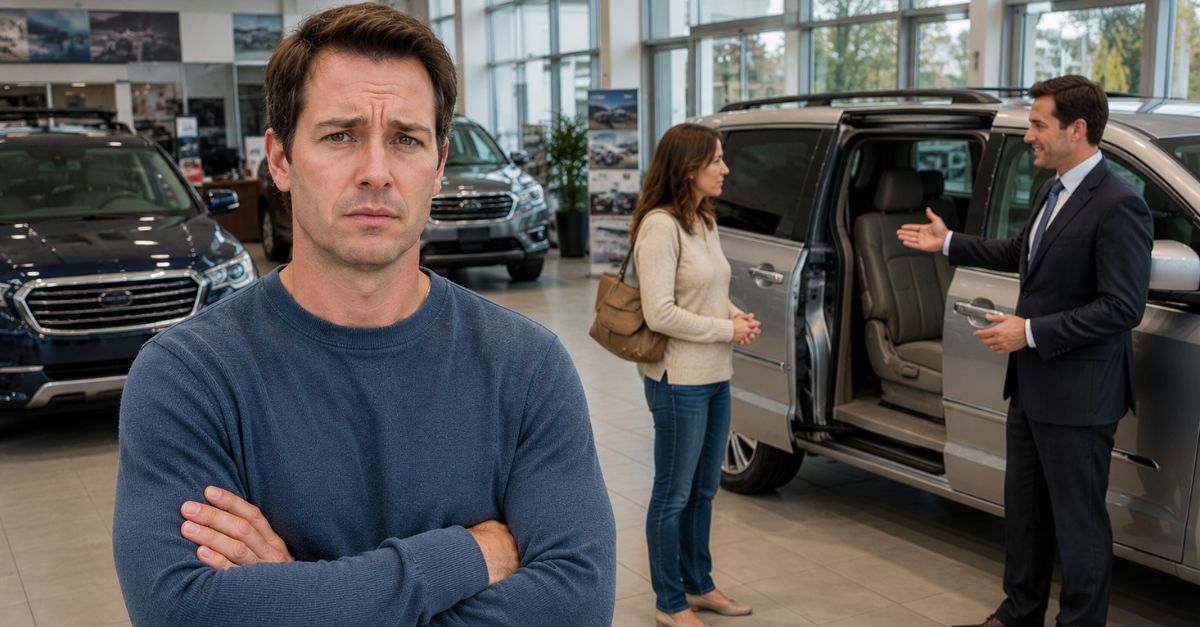

The Numbers Don’t Match, And Now You’re Paying For It

You signed the paperwork and drove off the lot thinking everything was locked in. But now the dealership is calling you back saying your income was listed incorrectly on the loan application, and suddenly the deal is falling apart. Their solution? Pay thousands more or return the car. It feels like the rug just got pulled out from under you. So what’s actually going on here, and what can you do about it? Let’s break it down.

This Happens More Often Than You’d Think

Believe it or not, this situation isn’t rare. Sometimes it’s a genuine mistake, and sometimes it’s something more questionable. Dealers have been known to inflate income or change details on loan applications to get financing approved in the first place.

Why Income Matters So Much

Your income is a key factor lenders use to decide whether to approve a loan and what terms to offer. If the number is higher than it should be, it can make a loan look safer than it actually is. That’s why even small changes can lead to big consequences later.

Honest Mistake Or Something More Serious

There are really two possibilities here. Either the dealership made an honest clerical error, or they knowingly changed your information to push the deal through. Figuring out which one you’re dealing with is the first step.

If It Was An Honest Mistake

Sometimes paperwork errors happen. Maybe someone typed the wrong number or misunderstood your income. If that’s the case, the lender may reject the loan once they verify your real financials, and the dealership has to fix the situation.

What To Do In The “Honest Mistake” Scenario

If it truly was a mistake, your best move is to slow things down and review everything. Ask for a copy of the application that was submitted and compare it to what you actually told them. If the numbers don’t match, you need to understand exactly how and why that happened before agreeing to anything new.

You Don’t Have To Accept Worse Terms Automatically

The dealership might push you to accept a higher interest rate or larger down payment. You are not obligated to agree right away. You can take time to explore other financing options or even walk away from the deal if it no longer makes sense.

You May Be Able To Unwind The Deal

If financing truly falls through, the dealership may have to cancel the deal entirely. That usually means returning the car and getting your deposit back. It’s not ideal, but it can be better than getting locked into a loan you can’t afford.

If The Dealer Changed Your Income On Purpose

This is where things get serious. If the dealership knowingly altered your income without your consent, that can be considered fraud or misrepresentation under consumer protection laws.

Why Dealers Do This

Some dealerships inflate income to get buyers approved for loans they wouldn’t normally qualify for. This helps close the sale, but it can leave you stuck with payments you can’t realistically afford.

You Could Actually Have A Case

If your income was falsified without your knowledge, you may have legal grounds to challenge the contract. In some cases, buyers have been able to unwind deals or even recover damages because of deceptive practices.

Don’t Let Them Pressure You Into Paying

If the dealer is saying “pay thousands more or give the car back,” that’s a pressure tactic. Take a step back. If fraud or misrepresentation is involved, they may not be in a position to enforce those demands as easily as they claim.

Ask For All Documentation

Request copies of everything, including the loan application, financing agreement, and any communications with lenders. This helps you see exactly what information was submitted and whether it matches reality.

Anastassia Anufrieva, Unsplash

Anastassia Anufrieva, Unsplash

Check What You Actually Signed

If the incorrect income appears on documents you signed, the situation gets more complicated. Signing doesn’t automatically mean you’re at fault, especially if you weren’t given a fair chance to review or understand the paperwork, but it does matter.

Consider Talking To The Lender Directly

Sometimes the lender isn’t aware of what happened at the dealership level. Contacting them directly can help clarify whether the loan was denied because of incorrect information and what your options are moving forward.

Get Legal Advice If Things Feel Off

If you suspect the dealership intentionally altered your information, it’s worth talking to a consumer protection or auto fraud attorney. Cases involving falsified loan applications can carry serious legal consequences for the dealer.

File A Complaint If Necessary

You can file complaints with agencies like the Federal Trade Commission or your state attorney general. This won’t fix everything overnight, but it can create pressure and document what happened.

Harrison Keely, Wikimedia Commons

Harrison Keely, Wikimedia Commons

Be Careful About Returning The Car

Before you hand the car back, make sure you understand the terms. Ask about your down payment, trade-in, and any fees. You don’t want to lose money unnecessarily because of their mistake.

Explore Your Own Financing

If you still want the car, consider securing financing independently through a bank or credit union. That can remove the dealership from the equation and give you more control over the terms.

So What Should You Do Right Now

Start by gathering your paperwork, reviewing the numbers, and figuring out whether this was a mistake or something more serious. From there, you can decide whether to renegotiate, walk away, or push back.

Final Thoughts

This situation feels overwhelming, but you’re not stuck with only the options the dealership is giving you. Whether it was an honest mistake or something more questionable, you have the right to question it, verify everything, and choose what works best for you. Take your time, stay informed, and don’t let pressure rush you into a bad deal.

You May Also Like: