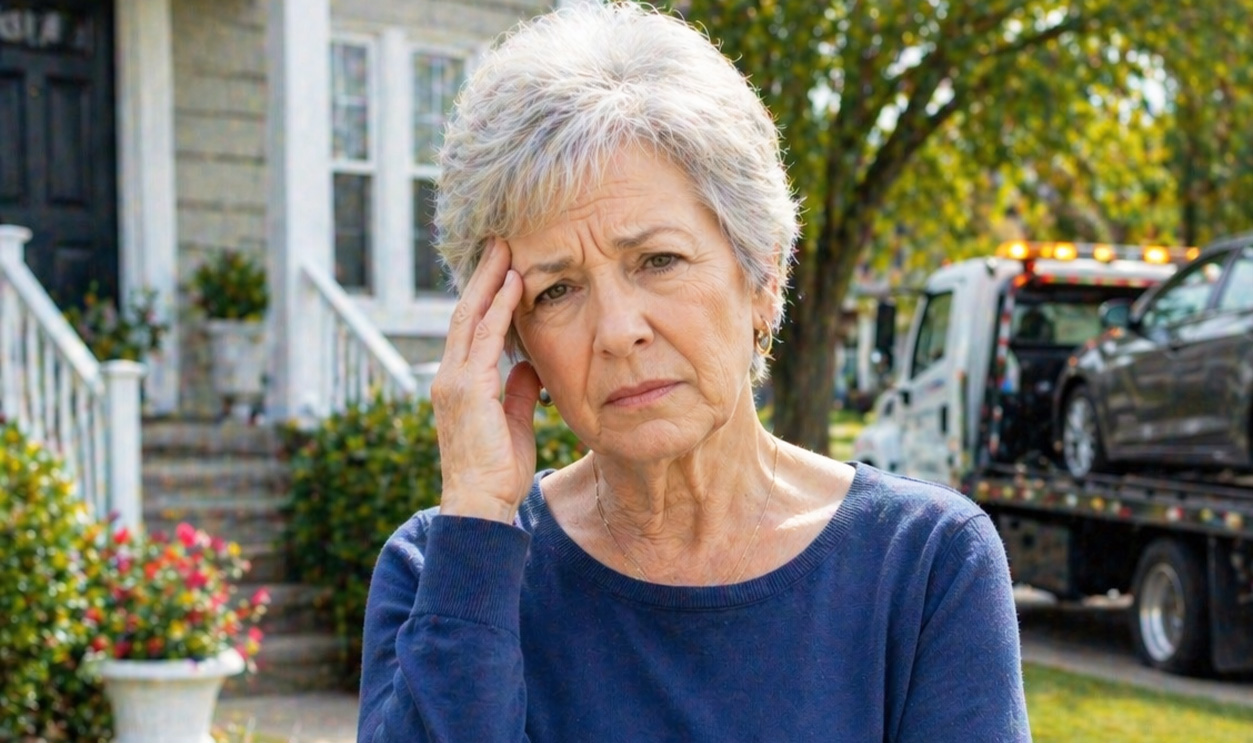

You Helped Them And Now You’re Paying For It

Co-signing a loan for a family member usually comes from a good place. You wanted to help them get approved and everything seemed manageable at the time. Fast forward, and the payments stopped, the car got repossessed, and now the lender is coming after you for the balance. Legally, co-signing puts you on the hook in a big way, but the good news is, you still have options to deal with the fallout.

You’re Legally Responsible

When you co-sign a loan, you’re not just a backup plan. You’re equally responsible for the debt. That means if the primary borrower stops paying, the lender can come directly to you for payment without chasing them first. It’s a tough position to be in, but understanding this is the first step toward taking control and figuring out a path forward.

Repossession Doesn’t Wipe Out The Debt

A lot of people assume that once the car is repossessed, the problem is over. It’s not. The lender will usually sell the car at auction, often for less than what’s owed. The remaining balance, called a deficiency, is what they’ll try to collect from you.

You Should Get A Notice Of Sale

After repossession, the lender is typically required to notify you about the sale of the vehicle. This notice should include details about when and how the car will be sold, and sometimes your right to redeem it by paying off the loan.

The Remaining Balance Can Be Significant

Because repossessed cars often sell for less than market value, the leftover balance can be surprisingly large. On top of that, fees for towing, storage, and the sale itself can get added to what you owe.

Don’t Ignore Calls Or Letters

It might be tempting to avoid the situation, especially if you’re frustrated with the family member involved. But ignoring the lender will only make things worse. They can escalate collections, damage your credit further, or even take legal action.

Check The Loan Agreement Carefully

Pull out the original loan documents and review them. Look at your obligations as a co-signer and any clauses about repossession and deficiency balances. Understanding the exact terms helps you know where you stand.

Verify The Numbers

Ask the lender for a full breakdown of what you owe. This should include the loan balance, sale price of the car, and any added fees. Mistakes can happen, and you don’t want to pay more than you actually owe.

You May Be Able To Negotiate

Lenders are often willing to negotiate, especially if you can offer a lump-sum payment. Settling the debt for less than the full amount isn’t guaranteed, but it’s worth asking about.

Payment Plans Are Often An Option

If paying the balance in full isn’t realistic, ask about setting up a payment plan. This can help you manage the debt without going into further financial trouble.

Your Credit Has Likely Taken A Hit

As a co-signer, the loan appears on your credit report. Missed payments and repossession can significantly lower your credit score. The sooner you address the debt, the sooner you can start repairing that damage.

You Can Go After The Primary Borrower

Even though the lender can collect from you, you may have the right to seek reimbursement from the person you co-signed for. This might involve working it out privately or, in some cases, taking legal action.

Be Realistic About Family Dynamics

Going after a family member for money is never easy. You’ll need to balance the financial impact with the personal relationship. Sometimes it’s worth trying to work out a repayment plan directly with them first.

Consider Legal Advice If The Amount Is Large

If you’re dealing with a significant balance, it may be worth speaking with an attorney. They can help you understand your rights, review the lender’s actions, and advise you on your options.

Watch For Collection Agencies

If the lender doesn’t collect directly, the debt may be sold to a collection agency. That doesn’t change your responsibility, but it can change how the debt is handled and negotiated.

Know Your Rights With Debt Collectors

If a collection agency gets involved, they must follow certain rules under federal law. They can’t harass you, misrepresent the debt, or use unfair practices. If they cross the line, you can file a complaint.

Bankruptcy Is A Last Resort

In extreme cases, bankruptcy might be an option to deal with overwhelming debt. This is a serious step with long-term consequences, so it’s something to consider carefully with professional advice.

Learn From The Situation

Co-signing can feel like a simple favor, but it carries real financial risk. Going forward, it’s important to treat co-signing like taking on the loan yourself, because that’s essentially what it is.

Can You Avoid Paying Altogether?

In most cases, no. If you signed the loan agreement, the lender has the right to collect from you. The focus usually shifts from avoiding the debt to managing it in the smartest way possible.

Final Thoughts

Co-signing a loan can come back to bite hard if things go wrong, especially when repossession enters the picture. While you can’t undo the agreement, you’re not stuck without options. By staying proactive, understanding your rights, and exploring negotiation or repayment strategies, you can get through the situation with as little damage as possible.

You May Also Like:

My friend says buying a car in cash is the worst way to do it. Is financing really that much better?