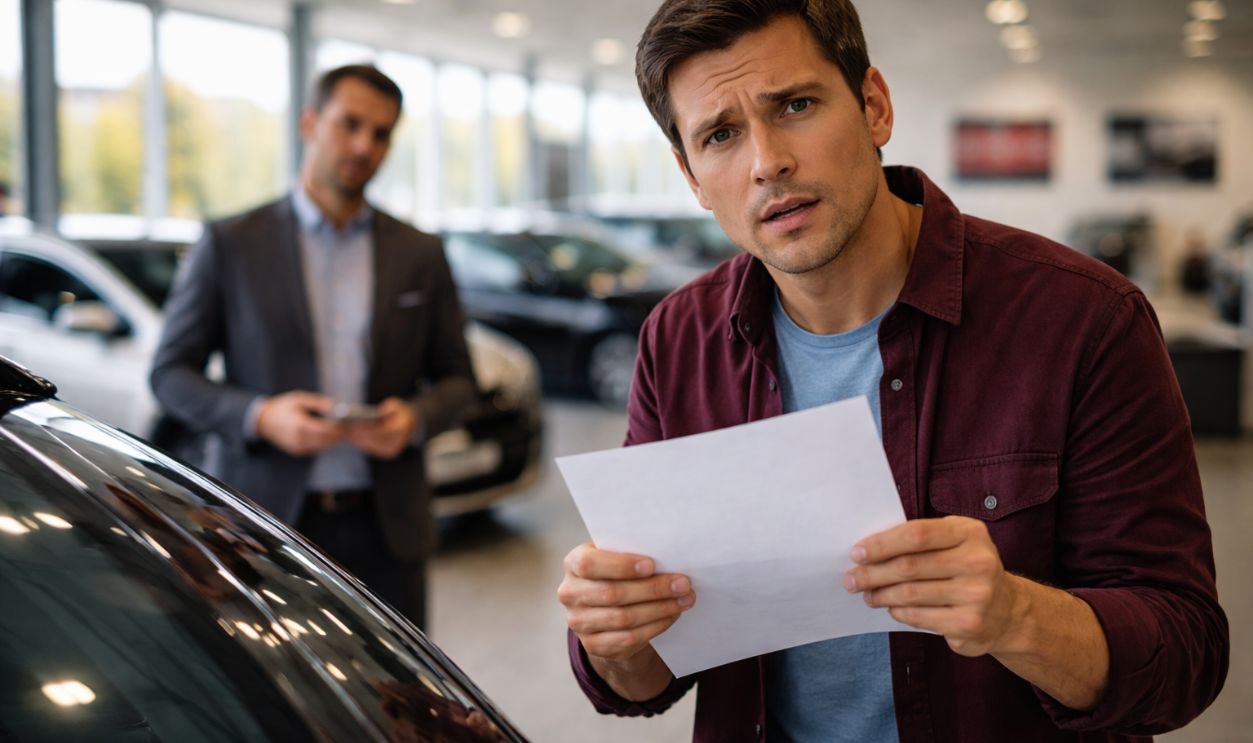

When A “Mandatory Warranty” Shows Up Out Of Nowhere

It’s an ugly surprise: You think you have a deal, then the dealership says a warranty or service contract is “required.” In a lot of cases, that add-on is not actually required by law, even if the salesperson says it is. Whether you can walk away depends on what you signed, whether financing is final, and whether your state gives you any cancellation rights. The main point is simple: dealers cannot make up legal requirements that do not exist.

First, Know What A Warranty Usually Means Here

When dealers say “warranty,” they often mean a vehicle service contract, not the carmaker’s original warranty. A service contract is a separate agreement that covers some repairs for a set time or mileage, usually for an extra cost. The Federal Trade Commission generally treats these as optional products, not automatic parts of every sale. That matters because optional products usually need your clear okay.

Dealers Often Bundle Add-Ons Into The Paperwork

Extended warranties, GAP coverage, tire protection, paint protection, and theft products often get mixed into the final paperwork. Some buyers do not notice them until the monthly payment jumps. The Consumer Financial Protection Bureau has warned that add-on charges can be rolled into auto loans and raise the total cost. If a dealer slipped one in without clearly explaining it, that is a serious warning sign.

“Mandatory” Can Be Misleading

A dealer may say a warranty is mandatory “for financing” or “for all used cars,” but that may be false or missing key facts. Under federal law, problems can come up when one product is tied to another, especially if the dealer falsely says the add-on is required. The FTC’s Used Car Rule also requires certain disclosures and helps buyers compare warranty terms. If the add-on was sold as required when it really was not, you may have grounds to refuse it or challenge the deal.

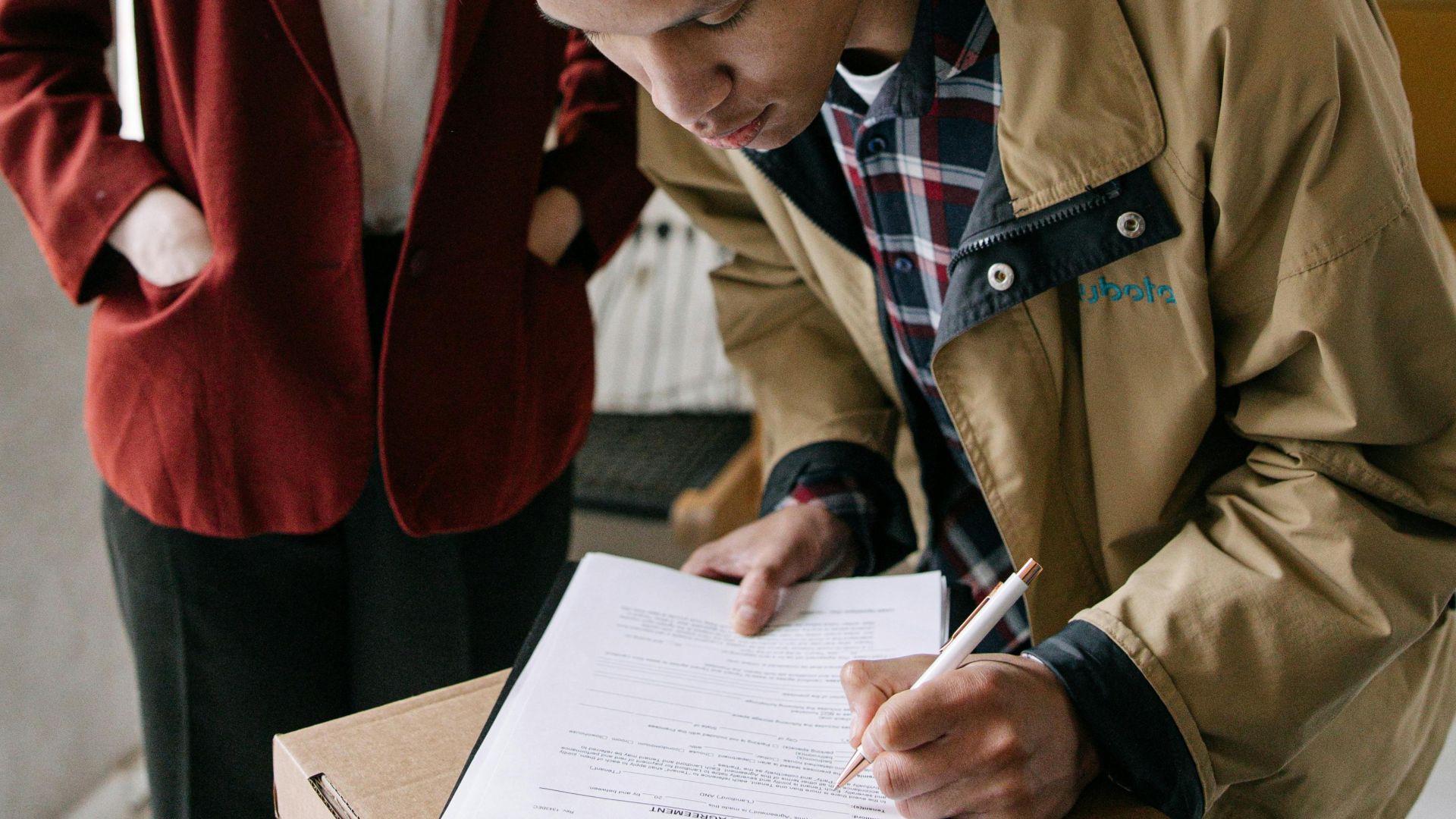

The Biggest Question: Did You Already Sign A Final Contract?

If you have not signed the retail installment sales contract or buyer’s order, walking away is usually much easier. At that point, you can just refuse the added warranty and decide not to go forward. If you already signed, things get more complicated because the signed papers control much of the deal. Your next step depends on whether the warranty appears in those documents and whether any cancellation language applies.

A Signed Contract Usually Matters More Than Verbal Promises

Car deals depend heavily on paperwork, and courts often start with the signed contract. If the contract includes the service agreement and shows a charge for it, the dealer may argue that you accepted it. Still, a signature does not automatically excuse fraud or deception. If the product was hidden, misrepresented, or added after you agreed to different terms, you may still have options.

There Usually Is No Automatic Three-Day Right To Cancel A Car Sale

This is one of the biggest myths in car buying. The FTC makes clear that the federal cooling-off rule usually does not apply to vehicle purchases made at a dealership. So if you are counting on a universal three-day cancellation right, that usually will not help. Any right to cancel will usually come from your contract, the service contract’s own terms, or state law.

But The Service Contract Itself May Be Cancellable

Even if the vehicle sale stands, the service contract may have its own cancellation terms. Many service contracts allow cancellation within a certain period for a full or partial refund, depending on timing and whether any claims were made. State insurance or consumer agencies often require specific disclosures about cancellation and refunds. So you may not be able to unwind the whole deal, but you may be able to remove the add-on and lower the financed amount or get a refund.

Look For These Documents Right Away

Get the retail installment contract, buyer’s order, service contract, warranty booklet, and any menu or list of add-on products. Check whether the service contract is listed separately and whether you initialed or signed next to it. Also look for arbitration clauses, cancellation sections, and any statement saying the product is required. The paperwork will show whether the dealership has a strong argument or a weak one.

Spot The Difference Between “Required By Lender” And “Dealer Wants It”

Lenders may require proof of insurance, but that usually does not mean they require an extended warranty or service contract. Truth in Lending rules are meant to make financed charges easier to see. If the dealer says the bank required the warranty, ask for that requirement in writing and ask for the lender’s name. A vague answer usually tells you plenty.

If Financing Isn’t Final, You May Still Have Leverage

Some deals are spot deliveries, which means you take the car home before financing is fully approved. If the lender later rejects the deal unless the terms change, you may be able to return the vehicle instead of accepting a more expensive contract. State laws differ, but unfinished financing can create a chance to renegotiate or unwind the deal. Read every conditional delivery or yo-yo sale document carefully.

Used Cars And Buyers Guides Matter Here

For many used cars sold by dealers, the FTC’s Used Car Rule requires a Buyers Guide that says whether the vehicle is being sold “as is” or with a warranty. The rule was updated to improve disclosures and help buyers understand warranty terms. A service contract is not the same thing as a dealer warranty, and the paperwork should not blur that line. If the Buyers Guide and the sales papers say different things, that is worth questioning.

Misrepresentation Can Change The Picture

If the dealership told you the warranty was legally required, required by the lender, or included for free when it was actually an extra charge, that can turn into a consumer protection issue. State unfair and deceptive practices laws often ban misleading statements in sales deals. The CFPB and FTC have both taken action in cases involving deceptive auto add-ons. That does not guarantee you will win, but it can strengthen your position.

Can You Walk Away Before Taking Delivery?

If you have not taken delivery and have not signed final papers, walking away is often the cleanest move. Calmly say you do not agree to the add-on and will not go forward unless it is removed. Ask for a revised buyer’s order showing the lower price without the service contract. If the dealer refuses, leave and keep copies or photos of any paperwork you were shown.

Can You Walk Away After Taking Delivery?

Once you have taken delivery and signed final documents, it is harder to cancel the entire sale just because you regret the add-on. Even so, if the contract was conditional, financing fell through, or the warranty was added through deception, you may still have room to challenge the transaction. Even if the sale stays valid, cancellation of the service contract may still be possible. Timing matters, so act fast.

How To Push Back Without Making Things Worse

Start calm and be specific: point out the exact charge, the document where it appears, and why you dispute it. Ask the finance manager to show where you agreed that the warranty was mandatory. Follow up in writing by email so there is a record. A clear paper trail is often more useful than arguing in the showroom.

Ask For A Full Breakdown Of The Out-The-Door Price

One of the smartest moves is to ask for an itemized out-the-door worksheet. That document should separate the vehicle price, taxes, registration, dealer fees, financing charges, and optional add-ons. If the “mandatory warranty” disappears when you ask for an itemized list, that is a good sign it was never mandatory in the first place. Clear numbers help.

Watch For Arbitration And Complaint Instructions

Many dealer contracts include arbitration clauses, which can affect how disputes are handled. That does not mean you have no rights, but it may mean you cannot go straight to court. Also check the service contract and sales paperwork for complaint contacts, administrator information, and cancellation steps. Missing a notice deadline can make a bad situation harder to fix.

Who To Contact If The Dealer Won’t Budge

If the dealership refuses to remove or cancel a wrongly added product, think about contacting your state attorney general’s office, state consumer protection agency, or state motor vehicle dealer regulator. You can also file complaints with the FTC and CFPB, especially if financing or deceptive add-ons are involved. If the service contract is overseen by your state insurance department, that agency may also help. These complaints can create pressure even if the dealer brushes you off at first.

Tony Webster, Wikimedia Commons

Tony Webster, Wikimedia Commons

When A Lawyer Is Worth The Call

If the charge is large, the facts suggest deception, or the dealership changed terms after you agreed, it may be worth calling a consumer law attorney. Many lawyers who handle auto fraud or unfair practices offer consultations. Bring every document, screenshot, and email, along with notes about what was said and when. Good records can make a maybe-case much stronger.

How To Protect Yourself On The Next Deal

Before signing, ask for the full contract packet in advance if possible and review the line items slowly. Do not rely on “it’s required” unless you can see that requirement in writing. Avoid rushed signing sessions and compare the monthly payment to the total amount financed, because add-ons often hide in that gap. If a dealer pressures you with fake urgency, that is usually your sign to pause or leave.

The Short Answer: Sometimes Yes, Sometimes No

If you never signed final paperwork or financing is not complete, you often can walk away from a deal that suddenly includes a “mandatory warranty.” If the sale is already final, you may not be able to cancel the whole purchase, but you may still be able to cancel the service contract or challenge deceptive conduct. The key is to read the documents, move quickly, and get everything in writing. A dealer can sell you a car, but it usually cannot force an optional add-on on you just by calling it “mandatory.”