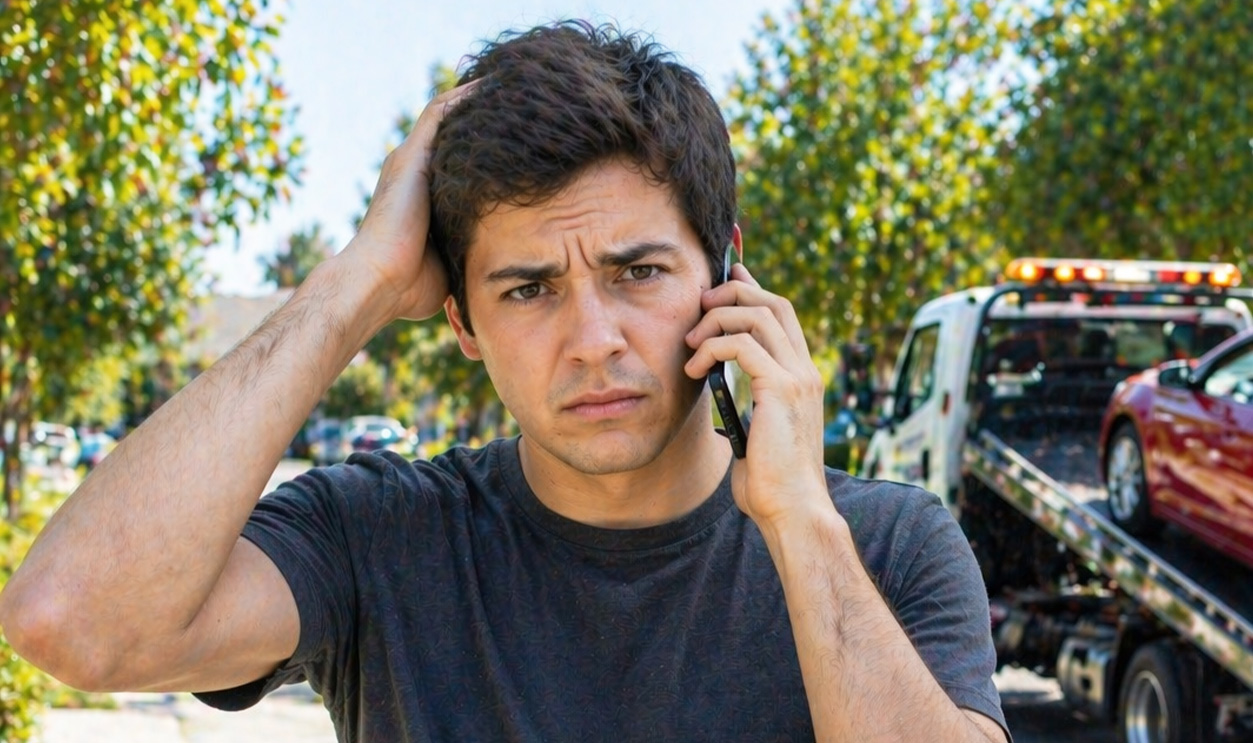

When Your Lender Doesn’t Stick To The Plan

You did what you were supposed to do: you talked to your lender, worked out a payment arrangement, and thought you had a plan in place to avoid repossession. Then out of nowhere, your car is gone anyway. No warning, no second chance, just a tow truck and a major headache. So what happened? And more importantly, what can you do now? Situations like this feel completely unfair, but you have more leverage than you think.

Don’t Assume It Was Allowed

Just because your car was repossessed doesn’t automatically mean the lender was in the clear. If you had a valid payment arrangement in place, especially one that was documented, the repossession could potentially be wrongful.

Verbal Agreements Can Be Tricky

If your arrangement was only discussed over the phone and never confirmed in writing, things get complicated. Lenders sometimes deny or reinterpret verbal agreements, which makes it harder to prove what was actually promised.

Written Agreements Carry More Weight

If you have emails, letters, or any written confirmation of the payment plan, that’s a big deal. Documentation showing the lender agreed to pause repossession or accept modified payments can strengthen your position significantly.

Check The Exact Terms Of The Arrangement

Not all payment arrangements fully stop repossession. Some are conditional, meaning you had to meet very specific deadlines or amounts. If even one condition wasn’t met exactly, the lender might argue they were still allowed to repossess.

Look At Your Payment History Closely

Go through your recent payments and compare them to the agreement. If you made payments on time and as agreed, that supports your case. If there were delays or partial payments, the lender may use that to justify their actions.

Contact The Lender Immediately

As soon as you realize what happened, reach out to your lender. Ask for a clear explanation of why the repossession occurred despite the arrangement. Keep the conversation focused and request everything in writing if possible.

Ask If The Repossession Can Be Reversed

In some cases, lenders may be willing to undo the repossession, especially if there was a misunderstanding or internal error. This could involve reinstating the loan and returning the vehicle once you bring the account current.

Understand Your Right To Reinstate Or Redeem

Depending on your state, you may have the right to reinstate the loan by catching up on missed payments or redeem the vehicle by paying off the full balance. These rights are time-sensitive, so acting quickly matters.

Get Details About The Sale Timeline

Lenders typically can’t sell your car immediately after repossession. There’s usually a waiting period, and you should receive notice before the sale. This window is your opportunity to take action if you want the car back.

Request A Breakdown Of What You Owe

Ask for a full accounting of your loan, including missed payments, fees, and repossession costs. This helps you understand what it would take to resolve the situation and also gives you a chance to spot any errors.

You May Be Able To File A Dispute

If you believe the repossession violated your agreement, you can dispute it directly with the lender. Provide copies of your payment arrangement and proof of payments. A strong, well-documented dispute can sometimes lead to a resolution.

Consider Filing A Complaint

If the lender isn’t responsive, you can file complaints with agencies like the Consumer Financial Protection Bureau or your state attorney general. This can sometimes push lenders to take a second look at your case.

Wrongful Repossession Is A Real Thing

If the lender repossessed your car despite honoring the agreement, it could be considered wrongful repossession. This doesn’t automatically mean you win, but it does mean you may have grounds to challenge their actions.

Legal Advice Might Be Worth It

If the situation involves a lot of money or feels clearly unfair, talking to a consumer protection attorney can help you understand your options. Sometimes a legal letter alone can change how a lender responds.

Don’t Forget About Your Personal Belongings

Even if the repossession stands, you still have the right to retrieve your personal items from the vehicle. Contact the repo company or storage lot as soon as possible to arrange pickup.

Centre for Ageing Better, Unsplash

Centre for Ageing Better, Unsplash

Watch For Credit Impact

A repossession can seriously affect your credit score. If you’re able to resolve the issue quickly or prove it was wrongful, you may be able to limit or even dispute the damage to your credit report.

Avoid Ignoring The Situation

It’s easy to feel overwhelmed and want to step back, but ignoring the issue can make things worse. The sooner you act, the more options you’ll have to fix or at least manage the situation.

Learn From The Fine Print

This situation highlights how important it is to get agreements in writing and understand the exact terms. It’s not just about making payments, it’s about knowing what protections you actually have.

So What Can You Do Right Now

Start by gathering your documents, reviewing your agreement, and contacting your lender for answers. From there, you can decide whether to dispute the repossession, try to get the car back, or focus on minimizing the financial damage.

Final Thoughts

Having your car repossessed after setting up a payment arrangement feels like the system failed you, and in some cases, it might have. But you’re not stuck without options. With the right documentation and a proactive approach, you may be able to challenge what happened or at least put yourself in a better position moving forward.

You May Also Like: