The Tempting Bad Idea

Your friend always seems to have a nice car, and he tells you that he skips a few loan payments on purpose so the lender cuts him a better deal. He may seem like he knows something you don't. In reality, he's being incredibly reckless, even if it has sometimes paid off.

The biggest problem is simple: once you miss payments, the damage can hit your credit and your options before any real negotiation even starts.

Why This Myth Keeps Spreading

The idea sticks around because lenders do sometimes negotiate with borrowers who are struggling. That part is true. What gets left out is that borrowers usually have a better shot at help before they go seriously delinquent, not after they stop paying on purpose.

What The CFPB Says About Trouble

The Consumer Financial Protection Bureau says borrowers who are having trouble paying an auto loan should contact the lender as soon as possible. The agency says some lenders may work with you on payment options or extensions depending on the situation. That is very different from deliberately missing payments to try to force a better deal.

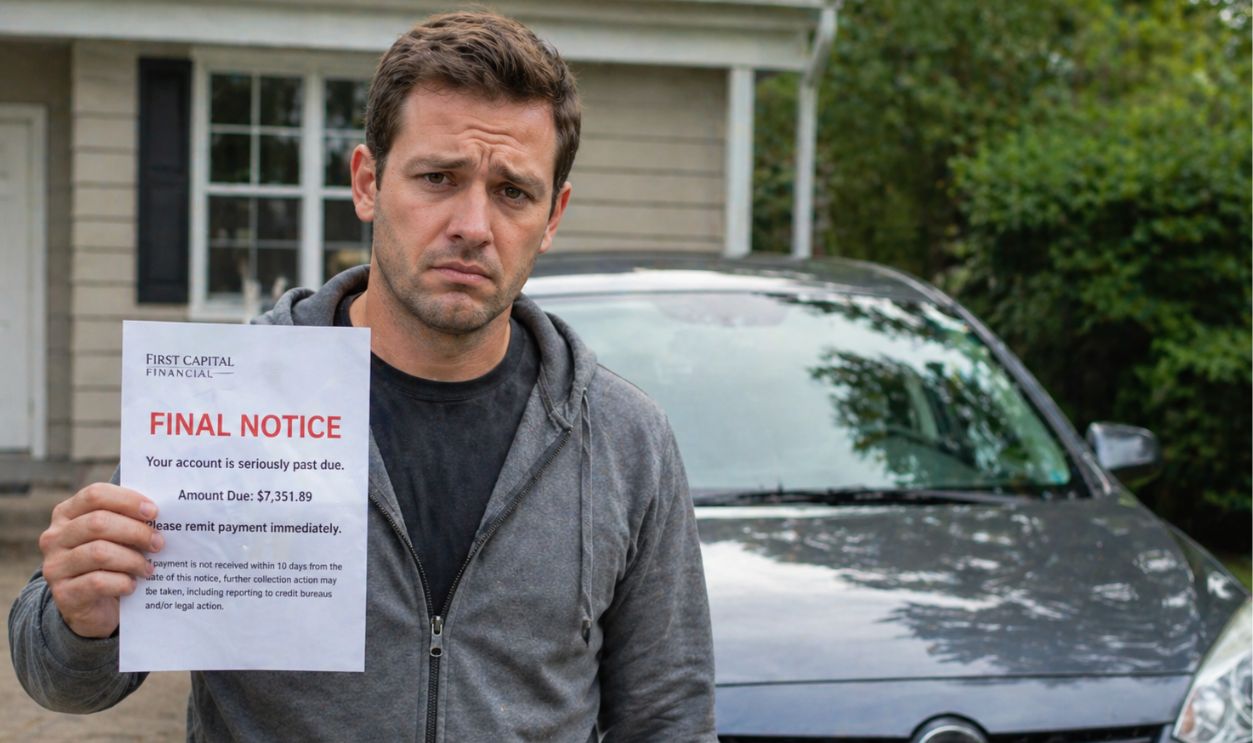

Late Is Not A Harmless Signal

A missed payment is not just a negotiating move. It can trigger late fees, extra interest, collection activity, and negative credit reporting. According to Experian, payment history is the biggest factor in most credit scores, so even one late payment can do real harm.

The 30-Day Line Matters

Many lenders charge a late fee once the grace period ends, but the bigger issue often starts at 30 days past due. Experian says payments generally may be reported as late to the credit bureaus once they are at least 30 days overdue. That means a plan to gain leverage can turn into a long-term credit problem fast.

Credit Damage Can Linger

A delinquent account does not just hurt for a month or two. The CFPB explains that negative information such as late payments can stay on your credit report for years. So even if a lender eventually agrees to a workout, the credit damage may outlast the short-term relief.

Your Bargaining Power Usually Shrinks

Here is what many people miss. Once you fall behind, the lender has more tools than you do, including repossession rights if the loan is secured by your vehicle. The National Consumer Law Center explains that auto lenders can repossess a car after default under state law rules, which means intentional delinquency can weaken your position instead of strengthening it.

Repossession Is Not A Bluff

With an auto loan, the car is the collateral. If the loan is in default, the lender may be able to repossess the vehicle without suing you first, depending on state law and whether it can be done without breaching the peace. That is a huge risk to take just to see whether a lender might negotiate.

You Can Still Owe Money After The Car Is Gone

Many drivers assume repossession wipes the slate clean. Often, it does not. The CFPB warns that after a repossession and sale, borrowers may still owe a deficiency balance if the car sells for less than the amount owed plus fees.

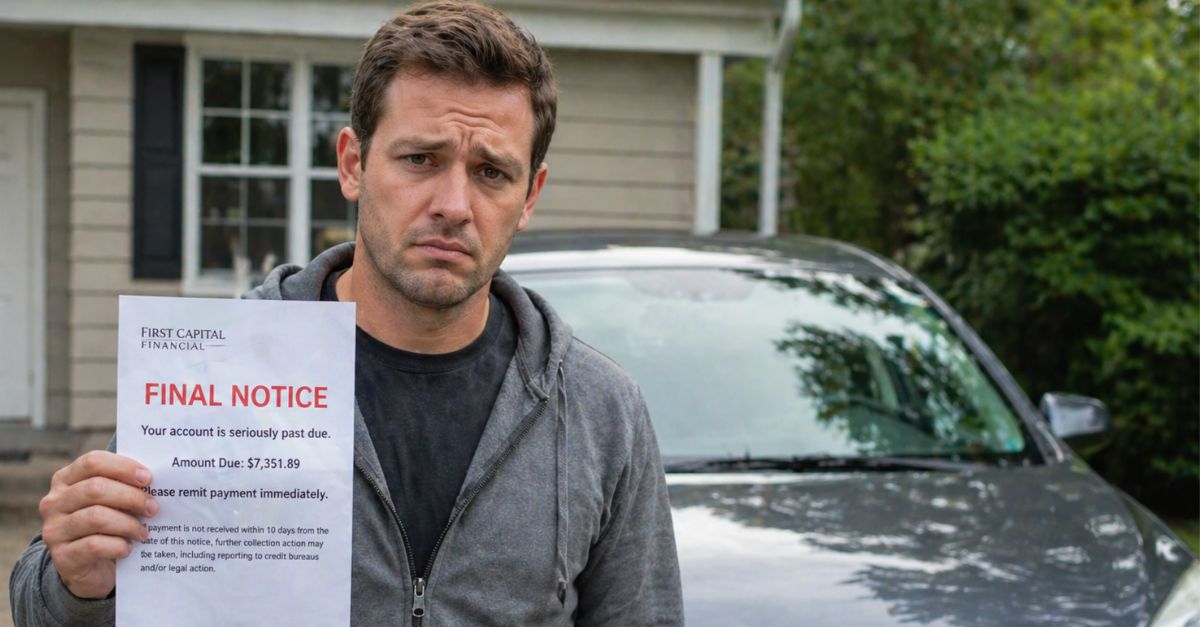

Fees Pile Up Faster Than Most People Expect

Intentional nonpayment can create a stack of costs. Late fees, collection costs, repossession expenses, storage charges, and legal fees may all enter the picture. What started as an attempt to save money can quickly become a much more expensive loan problem.

There Is A Grain Of Truth Here

Some lenders do offer hardship programs, deferred payments, loan modifications, or payment extensions. That is the small piece of truth keeping this advice alive. But those programs are generally meant for borrowers who speak up early and document hardship, not for people trying to game the system.

What Lenders Actually Want

Lenders usually want steady repayment, not chaos. If you call before missing payments, explain the issue, and ask about hardship help, you are showing that you are trying to solve the problem. That is far more convincing than silence followed by delinquency.

Timing Can Change The Outcome

The difference between calling before a payment is due and calling after 60 days of missed payments can be huge. Early contact may preserve more options, including temporary relief that avoids credit damage. Waiting can push your account deeper into collections, where flexibility is often lower.

What To Ask For Instead

If money is tight, ask about a payment extension, due date change, short-term forbearance, repayment plan, or hardship review. You can also ask whether the lender will waive a fee or allow partial payments. Those are specific requests that have a better chance of helping than an intentional missed payment.

Get Any Promise In Writing

If a lender offers help, ask for the terms in writing before assuming you are protected. You need to know whether interest still builds, whether the payment is simply postponed, and whether the account will be reported as current or delinquent. A vague phone promise is not enough when your car and credit are on the line.

Refinancing Can Be The Safer Move

If your credit is still decent and rates have improved for your profile, refinancing may lower the payment without triggering default. The Federal Trade Commission advises shoppers to compare total financing costs, not just the monthly payment. Stretching out the loan can shrink the bill each month while increasing the total interest paid.

Selling The Car May Beat Falling Behind

If the payment is crushing your budget, selling the vehicle or trading down can be smarter than sliding into delinquency. It is not fun advice, but it can keep a bad situation from getting worse. The key is acting before missed payments hurt your credit and before the vehicle loses more value.

Voluntary Surrender Is Still Serious

Some borrowers think handing the car back voluntarily is softer than repossession. It may reduce some hassle, but it does not erase the debt consequences. You may still owe a deficiency balance, and the account can still damage your credit history.

The Debt Collector Problem

Once an account is seriously delinquent, collection calls and letters may follow. At that point, your goal often shifts from trying to negotiate a better loan to limiting the fallout. That is not a stronger bargaining position. It is damage control.

What If You Truly Cannot Pay

If the hardship is real, the answer is not to fake distress by skipping payments. The answer is to contact the lender right away, review your budget, and document what changed, such as job loss, medical bills, or another emergency. The CFPB specifically encourages borrowers to ask about available help as soon as trouble appears.

Watch Out For Street-Corner Finance Advice

Money myths spread because somebody knows somebody who skipped payments and got a deal. What you usually do not hear is the rest of the story, including the credit damage, fees, or how close they came to losing the car. A one-off anecdote is not a solid financial strategy.

State Law Can Make Things Worse Or Faster

Repossession rules vary by state, but that does not make deliberate delinquency safe. The National Consumer Law Center notes that state law controls many repossession and notice rules. Depending on where you live, things can move quickly once you are in default.

Your Credit Future Matters More Than One Bill

A lower payment today can cost you much more later if your credit score drops. Negative marks can affect future car loans, credit cards, apartment applications, and sometimes even insurance pricing. That is a steep price to pay for a tactic that often does not deliver the promised leverage.

There Is A Better Negotiation Script

A smarter approach is to call the lender before the due date, explain the hardship clearly, and ask for specific options. Keep notes with dates, names, and what was offered. If the first representative cannot help, politely ask whether there is a hardship department or a supervisor who can review your case.

Red Flags In Any Advice

Be skeptical of anyone who says there is no downside to missing payments. Be just as skeptical if they cannot explain when the lender reports late payments, what default means under your contract, or how repossession and deficiency balances work. If the advice skips those details, it is probably bad advice.

The Bottom Line

So, is intentionally missing payments to negotiate a better loan real or reckless? There is a small kernel of reality because lenders may negotiate with borrowers who are in trouble, but the tactic itself is usually reckless. If you need relief, ask early, get the terms in writing, and protect your credit before a bad month turns into a much bigger financial mess.