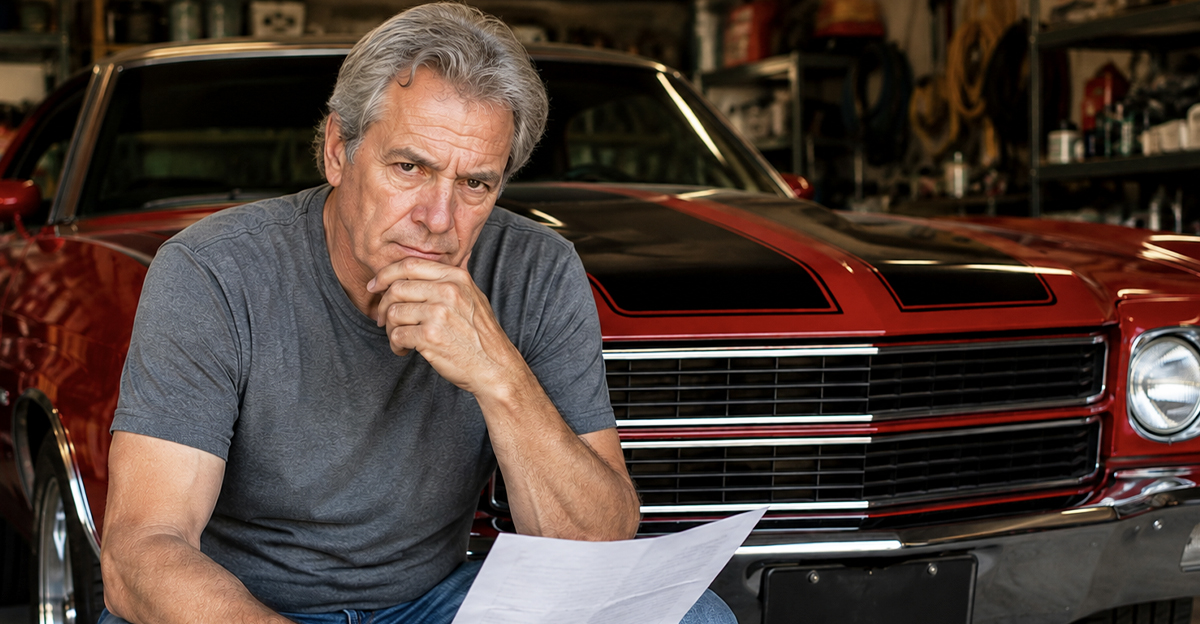

I Finally Finished The Restoration, And Then The Insurance Problems Started

Restoring a classic car is often a labor of love that takes years of work, countless hours, and a surprising amount of money. Many owners assume the hard part ends when the restoration is complete and the car is finally back on the road. Then they call an insurance company and discover that getting proper coverage is far more complicated than insuring a modern vehicle. The good news is that classic cars can absolutely be insured, but they often fall into a completely different insurance world than ordinary daily drivers.

Classic Cars Are Not Insured Like Regular Cars

One of the biggest surprises for first-time classic car owners is that standard auto insurance policies are often a poor fit. Traditional insurance is designed around everyday vehicles that gradually lose value over time. Classic cars frequently do the opposite, especially after extensive restoration work. That difference forces insurers to approach them very differently from normal commuter vehicles.

SG2012, CC BY 2.0, Wikimedia Commons

SG2012, CC BY 2.0, Wikimedia Commons

Determining The Value Is Surprisingly Difficult

A modern car's value can usually be estimated using sales data, depreciation schedules, and market guides. A restored classic car is often much harder to value accurately. Two vehicles of the same make, model, and year may have dramatically different values depending on restoration quality, originality, documentation, rarity, and market demand. That uncertainty makes insurers cautious.

Restoration Costs Often Exceed Market Guides

Many owners discover that they have invested far more money into a restoration than standard pricing guides suggest the car is worth. Parts, labor, paint work, body repairs, engine rebuilding, and specialty services can add up quickly. Insurance companies may not automatically accept the owner's estimate of value simply because that amount was spent. Proving the vehicle's true worth often becomes a major part of the process.

Agreed Value Coverage Changes Everything

Many classic car policies use something called agreed value coverage. Under this arrangement, the owner and insurer agree on the vehicle's value before a loss occurs. If the vehicle is totaled under covered circumstances, that agreed amount generally becomes the payout rather than a depreciated market value. This is one reason many enthusiasts seek specialty classic car insurance instead of relying on standard policies.

Insurance Companies Want Proof

If you claim your restored vehicle is worth $75,000, $100,000, or more, the insurer will usually want evidence supporting that figure. Restoration receipts, photographs, appraisals, auction results, and documentation often become important. The stronger your records are, the easier it becomes to justify the value you are requesting.

Photos Become Extremely Important

Many classic car insurers require extensive photographs during the application process. They may want images of the exterior, interior, engine bay, trunk, chassis, and other components. These photos help establish the vehicle's condition before coverage begins. They can also become useful later if questions arise after a claim.

Appraisals Are Sometimes Required

Some insurers require professional appraisals before issuing coverage on high-value vehicles. A qualified appraiser can evaluate the condition, originality, restoration quality, and market value of the car. While appraisals cost money, they often help eliminate disputes later by creating an independent assessment of the vehicle's worth.

Not Every Old Car Qualifies

Many people assume that any older vehicle automatically qualifies as a classic car. Insurance companies often have their own definitions and requirements. Age is important, but factors such as condition, rarity, collectibility, and intended use frequently matter as well. A neglected old vehicle may not qualify for the same coverage options as a carefully restored collector car.

Daily Driving Can Be A Problem

One reason classic car insurance is often cheaper than standard insurance is that insurers expect the vehicle to be driven less frequently. Many specialty policies include mileage restrictions or usage limitations. Owners who plan to use the vehicle as a daily commuter may discover that certain collector-car policies are unavailable to them.

Storage Requirements Are Common

Many insurers want classic cars stored in secure locations when not being driven. Garages, enclosed storage facilities, and other protected locations are often preferred. Some companies may refuse coverage or charge higher premiums if the vehicle is routinely parked outdoors. Storage conditions play a bigger role than many first-time owners expect.

Modifications Can Complicate Coverage

Restorations do not always focus on factory-original specifications. Many owners install upgraded engines, modern brakes, custom wheels, aftermarket suspension systems, or other modifications. While these upgrades may improve performance, they can make valuation and underwriting more difficult. Insurers often want detailed information about any significant modifications.

Originality Can Affect Value

In the collector-car world, originality often influences value significantly. Some buyers and insurers place enormous importance on matching numbers, factory-correct components, original paint colors, and documented history. A beautifully restored vehicle may still be valued differently if it departs substantially from its original configuration.

Parts Availability Worries Insurers

Repairing a modern vehicle usually involves ordering replacement parts from established suppliers. Classic cars present a different challenge. Certain parts may be rare, discontinued, custom-fabricated, or extremely expensive. Insurance companies understand that even relatively minor repairs can become complicated when replacement components are difficult to obtain.

Repair Costs Can Be Shockingly High

Many people underestimate how expensive classic car repairs can be. Specialized bodywork, rare parts, vintage trim pieces, custom paint matching, and restoration-quality labor often cost significantly more than repairs on modern vehicles. Insurers take those potential costs into account when evaluating coverage and premiums.

Theft Risk Is A Real Concern

Classic cars can be attractive targets for thieves. Some vehicles are stolen intact, while others are targeted for rare parts that can be difficult to trace. Certain models are especially desirable because of their collector value. Insurers often evaluate theft risk carefully when underwriting collector vehicles.

Documentation Can Save You Thousands

One of the smartest things a restoration owner can do is keep detailed records throughout the project. Save receipts, photographs, invoices, appraisal reports, build sheets, and correspondence related to the restoration. These records help establish both the quality of the work and the amount invested. They can become invaluable during valuation disputes.

Auction Results Influence Values

Insurance companies often look at recent sales data when evaluating classic vehicles. Auction houses such as Barrett-Jackson, Mecum, and RM Sotheby's provide publicly available examples of what similar vehicles have sold for. These results can support or challenge the value an owner is claiming. Market trends often play a major role in coverage decisions.

InSapphoWeTrust, CC BY-SA 2.0, Wikimedia Commons

InSapphoWeTrust, CC BY-SA 2.0, Wikimedia Commons

Values Can Change Quickly

Unlike most daily drivers, classic cars may appreciate significantly over time. A policy that was appropriate five years ago may no longer provide adequate protection today. Owners who fail to update their coverage sometimes discover that their insured value no longer reflects current market conditions. Periodic reviews are extremely important.

Specialty Insurers Often Understand Classics Better

Many mainstream insurance companies offer classic vehicle coverage, but specialty insurers often focus specifically on collector vehicles. These companies may have more experience with agreed-value policies, restoration projects, rare models, and collector-car claims. For many owners, the extra expertise makes the process much smoother.

SG2012, CC BY 2.0, Wikimedia Commons

SG2012, CC BY 2.0, Wikimedia Commons

Claims Can Become More Complicated

A claim involving a restored classic car often requires more investigation than a claim involving a typical commuter vehicle. Valuation disputes, repair methods, parts sourcing, and restoration standards can all become points of discussion. The complexity is one reason proper documentation before a loss is so important.

Underinsuring The Car Is A Common Mistake

Some owners focus heavily on keeping premiums low and end up insuring the vehicle for far less than its true value. That may save money initially, but it can create major problems after a serious loss. If the car is totaled, inadequate coverage may leave the owner with only a fraction of what the vehicle was actually worth.

The Insurance Company Is Not Trying To Punish You

Many first-time collectors become frustrated when insurers ask dozens of questions, request photographs, demand appraisals, or require proof of storage. While the process can feel excessive, the insurer is often trying to determine how to value a highly unusual asset. A restored classic car presents risks and valuation challenges that simply do not exist with ordinary vehicles.

The Restoration Is Only Part Of The Journey

Finishing a restoration feels like reaching the finish line, but ownership comes with additional responsibilities. Proper valuation, documentation, storage, maintenance, and insurance all become part of protecting the investment. The more effort you put into these areas, the less likely you are to face unpleasant surprises later.

The Extra Work Can Be Worth It

Getting insurance for a restored classic car often feels far more difficult than insuring a modern vehicle because the stakes are higher and the values are harder to determine. Insurers need to understand exactly what they are covering and what it would cost to replace or repair. While the process can be frustrating, the right coverage can protect years of hard work and potentially save you from a devastating financial loss if something goes wrong.

You May Also Like:

_-_14453314104.jpg){kind=link}

.jpg){kind=link}

{kind=link}