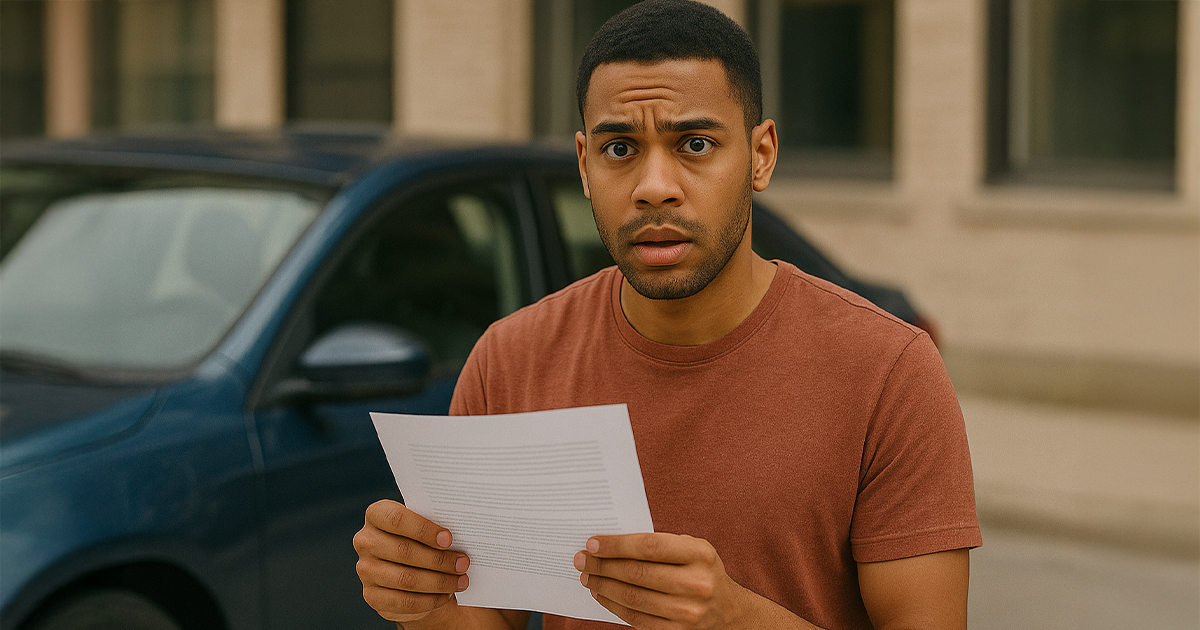

Insurance Shot Up—Now What?

Your car insurance just doubled, but you’re still stuck paying off a long car loan. You didn’t sign up for this kind of monthly pressure. You can’t ditch the car, and you can’t ditch the insurance. So what now?

Take a Breath, Then Check the Numbers

First, breathe. You’re not the only one this is happening to. Start by writing down your new monthly insurance premium, car payment, and total monthly expenses. Then look at what’s coming in. See where every dollar is going—clarity first, then solutions. The clearer the picture, the easier it’ll be to figure out next steps without feeling totally overwhelmed.

Review Your Coverage

Call your insurance company and ask for a full breakdown of your coverage. Are you paying for extras like roadside assistance, rental reimbursement, or low deductibles? Can you raise your deductible to lower your monthly bill? Small tweaks can lead to big savings. Don’t be afraid to ask questions—it’s your money.

Shop Around, Even Mid-Policy

You don’t have to wait until your policy ends. Get quotes from other insurance companies now. Many allow you to switch mid-policy without a penalty. Some may offer better rates for the same coverage. Just make sure you don’t cancel your current policy until the new one is active to avoid a lapse.

Look Into Discounts

Ask about any and all discounts—good driver, student, military, multi-car, bundling with renters or home insurance, or even safe driving app programs. Companies don’t always advertise these, and they can stack. Even $10–$20 saved per month adds up to a few hundred a year.

Call Your Loan Provider

Talk to your lender. You can’t just stop paying, but you might be able to extend your loan term or refinance to lower the monthly payment. Even if the overall cost goes up, a lower monthly bill could make a big difference right now. Just make sure the math works for you.

Rework the Rest of Your Budget

Start trimming spending in other areas. Go through subscriptions, dining out, streaming services, or anything non-essential. Even cutting $100 from various places can free up cash. Use budgeting tools or apps if it helps. This doesn’t have to be forever—just until you rebalance.

Set Up a Car Emergency Fund

Try to stash $10–$20 per week in a separate savings account just for car expenses. Even if things feel tight, small amounts add up. This can help cover unexpected rate hikes, repairs, or fees later on, so you're not stuck relying on credit cards.

Try Usage-Based Insurance

Some insurers offer pay-per-mile or usage-based programs that track how often and how safely you drive. If you work from home or don’t drive much, you could save big. It’s usually easy to enroll and doesn’t require a full policy switch.

Increase Your Income (Temporarily)

Pick up a side hustle or gig just until you feel more stable. Even $200 extra per month can plug the gap. Look into delivery apps, freelance work, or online gigs that fit your schedule. It doesn’t have to be long-term—just enough to help you reset.

Check Your Credit Score

Insurance rates often use credit-based pricing. If your credit recently dipped, your rate might’ve spiked. Pull your report for free and look for errors. Paying off debt, making on-time payments, and limiting new credit inquiries can help improve your score and lower your premium over time.

Consider a Different Car—Eventually

Right now, you’re locked in. But when the loan ends, choose your next vehicle carefully. Insurance tends to be cheaper on older, safer, and less flashy cars. Look up average insurance costs before you buy. It can save you hundreds a year.

See if You Qualify for State Help

Some states offer low-cost auto insurance programs for drivers with low income. It’s worth a quick search to see if you qualify. The programs vary, but they’re designed to make basic coverage more affordable.

Talk to Someone

If all this feels like too much, talk to a nonprofit credit counselor. They’ll help you sort out your budget, understand your options, and plan next steps. It’s free or low-cost, and way less stressful than going it alone.

Don’t Let It Snowball

Don’t let the pressure push you into putting insurance on a credit card or skipping bills. That creates a new problem. Tackle this one with a clear head. Use your budget and new strategy to stay in control before things spiral.

Stay Organized

Use a spreadsheet, budgeting app, or even a notebook to track your car expenses, insurance payments, and loan balance. Knowing when things are due—and how much—is half the battle. Organization turns chaos into something manageable.

Plan for the Next Renewal

Make a note to check rates 30–45 days before your policy renews. That’s the best time to compare quotes and negotiate. Set a reminder in your phone. Insurance companies count on people staying put—use that to your advantage.

Final Thought: You’ve Got Options

It might feel like your budget exploded, but you’re not powerless. With a few smart moves, a little trimming, and maybe some temporary hustle, you can work through this. You’ve got options—and one step at a time is enough."

You May Also Like:

My check engine light went off by itself. Should I still take it in?

DIY Car Maintenance That Anyone Can Do

Weird Car Sounds You Shouldn’t Ignore