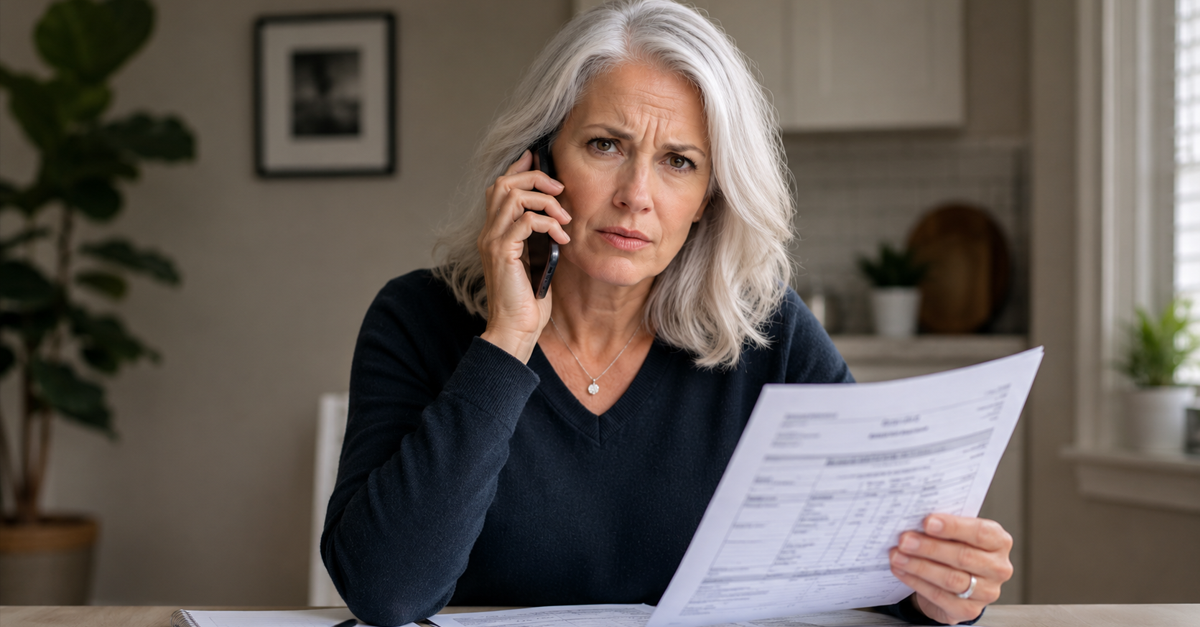

The Charges That Wouldn’t Stop

You canceled your car insurance, got the confirmation email, and thought you were done. Then another payment hit your bank account, followed by another, leaving you trapped in a customer service nightmare over charges that never should have happened. It is more common than many drivers realize, but there are ways to stop the withdrawals and fight to get your money back.

Why Insurance Billing Problems Happen

Insurance companies process millions of payments every month. Most policies are tied to automatic electronic funds transfers, debit cards, or recurring credit card charges. When a cancellation request gets mishandled, the payment system sometimes keeps running. In some cases, the insurer claims the cancellation was incomplete. Other times, billing departments and customer service teams fail to communicate properly. That can leave drivers stuck paying for coverage they no longer have.

Your First Step Is Gathering Evidence

Before contacting anyone, collect every document related to the cancellation. Save emails, screenshots, cancellation confirmations, chat logs, and bank statements showing the withdrawals. If you mailed paperwork, locate tracking numbers or delivery receipts. Strong documentation can make the difference between a quick refund and a months-long fight. Insurance companies respond much faster when consumers provide precise dates and records.

Check Whether The Policy Was Actually Canceled

Many drivers assume a verbal cancellation is enough. Some insurers require signed forms, written notice, or confirmation from an agent before the cancellation becomes official. If one step was missed, the company may argue the policy stayed active. Review your policy documents carefully. Look for sections labeled “Cancellation” or “Termination.” Those rules explain what the insurer requires before stopping billing.

Understand The Difference Between Cancellation And Nonrenewal

Cancellation ends a policy before the expiration date. Nonrenewal means the policy naturally expires and is not renewed for another term. Confusing the two can create billing problems. If you simply stopped paying without formally canceling, the insurer may have continued charging fees or reporting missed payments. Always make sure you receive written proof that the policy officially ended.

Automatic Payments Can Become A Trap

Autopay is convenient until something goes wrong. Once recurring withdrawals are linked to your bank account, insurers can continue pulling money unless the authorization is revoked correctly. Some drivers mistakenly believe canceling the policy automatically cancels autopay authorization. That is not always true. You may need to separately revoke permission for electronic withdrawals.

Federal Law Gives Consumers Protections

The Electronic Fund Transfer Act protects consumers from unauthorized electronic bank withdrawals. If a company continues taking money after permission has been revoked, consumers can dispute those charges with their bank. Banks must investigate reported errors within specific timeframes. Consumers also have the right to stop preauthorized electronic payments by notifying their bank at least three business days before the next scheduled withdrawal.

Start With The Insurance Company

As frustrating as it sounds, the first move should still be contacting the insurer directly. Ask for a supervisor or billing specialist rather than a general customer service representative. Calm persistence usually works better than anger. Request written confirmation that the policy is canceled and ask for a detailed refund timeline. Always record the date, time, and name of every representative you speak with.

Never Rely On Verbal Promises Alone

Customer service agents often say refunds are “processing” or “pending.” Without written confirmation, those promises may go nowhere. Ask for an email summarizing every conversation. If they refuse, send your own follow-up email documenting what was discussed. That creates a paper trail you can use later if the dispute escalates.

Banks Can Stop Future Withdrawals

If the insurer keeps charging you, contact your bank immediately. Request a stop payment order for future automatic withdrawals. Most banks can block recurring debits from a specific company. There may be a fee for the stop payment request. However, that fee is usually much smaller than months of continued unauthorized withdrawals.

You May Also Need To Close The Payment Authorization

Stopping one payment is not always enough. Some insurers reattempt withdrawals under slightly different transaction codes. Ask your bank whether you should revoke ACH authorization entirely. In severe cases, consumers sometimes close the affected bank account and open a new one. That is inconvenient, but it completely cuts off future drafts.

Credit Card Payments Offer Extra Protection

Drivers who paid with a credit card often have stronger dispute rights than those who used debit cards or bank transfers. The Fair Credit Billing Act allows consumers to dispute unauthorized charges. Credit card issuers frequently reverse disputed charges quickly while they investigate. That can provide faster relief than waiting for an insurance company refund.

Timing Matters In Billing Disputes

Most banks and card issuers impose deadlines for reporting unauthorized transactions. Waiting too long can weaken your claim. Review your statements every month so problems are caught early. Many financial institutions require disputes within 60 days of the statement date. Filing promptly gives you the strongest legal protections.

State Insurance Departments Can Help

Every state has a department or commissioner that regulates insurance companies. If customer service ignores you, filing a formal complaint can get attention fast. Insurance regulators track complaint patterns and often contact insurers directly. Companies usually respond much faster when a regulator becomes involved.

Filing A Complaint Is Easier Than You Think

Most state insurance departments allow online complaints. You typically submit your policy number, cancellation evidence, and a summary of the problem. Attach supporting documents whenever possible. Be factual and organized. Emotional language is less effective than a clear timeline showing exactly what happened.

The Better Business Bureau Is Another Option

The Better Business Bureau does not regulate insurers, but many companies respond quickly to public complaints there. Businesses dislike unresolved BBB disputes because they affect reputation scores. A detailed complaint sometimes triggers outreach from higher-level customer service departments. That can succeed when normal phone support fails.

Social Media Can Get Attention Fast

Public complaints on platforms like X, Facebook, or Reddit sometimes produce surprisingly quick responses. Insurance companies closely monitor social media because negative posts can spread rapidly. Stick to facts and avoid insults or threats. A professional tone increases the chances that the company will respond constructively.

Keep Detailed Notes During Every Call

Create a running log with dates, representative names, phone numbers, and conversation summaries. If the dispute drags on, that record becomes extremely valuable. Detailed notes help expose contradictions between different customer service agents. They also strengthen complaints filed with banks or regulators.

Ask For Specific Refund Dates

Do not accept vague phrases like “soon” or “in process.” Ask exactly when the refund will be issued and how it will be delivered. Push for concrete deadlines. If the representative cannot answer, escalate to a supervisor immediately. Unclear timelines often signal internal confusion.

Some Refunds Take Longer Than Expected

Insurance refunds sometimes require underwriting review or accounting approval. That process can take several weeks. However, unexplained delays beyond one billing cycle deserve closer scrutiny. Ask whether the refund will include all unauthorized charges, taxes, and fees. Partial refunds are another common problem.

Beware Of Cancellation Fees

Some insurers charge short-rate cancellation fees if a policy ends before the term expires. These fees are usually disclosed in the policy contract. Even when fees are allowed, the insurer cannot keep charging you indefinitely after cancellation. Make sure any deductions match the actual policy terms.

Vodafone x Rankin everyone.connected, Pexels

Vodafone x Rankin everyone.connected, Pexels

Small Claims Court Is Sometimes Necessary

If the insurer refuses to refund your money, small claims court may be an option. These courts are designed for relatively simple disputes involving limited dollar amounts. Bring organized evidence, including cancellation records and bank statements. Many companies settle before the hearing once formal legal action begins.

Arbitration Clauses May Affect Your Options

Some insurance contracts include mandatory arbitration clauses. That means disputes must go through private arbitration instead of court. Read your policy carefully to understand your rights. Arbitration procedures vary depending on the insurer and state laws.

Class Action Lawsuits Occasionally Happen

When many customers experience the same billing issue, law firms sometimes pursue class action lawsuits against insurers. These cases often involve unauthorized withdrawals or deceptive billing practices. You can search online to see whether your insurer has faced similar complaints. A pattern of consumer issues may strengthen your case.

Emotional Stress Is Part Of The Problem

Financial disputes with large companies can feel exhausting. Repeating your story to different representatives and watching money disappear each month creates real stress. Taking organized, step-by-step action helps restore a sense of control. The more documentation you gather, the stronger your position becomes.

Persistence Usually Wins

Insurance companies count on some customers giving up. Staying organized and persistent often makes the biggest difference. Escalate methodically instead of emotionally. Many consumers eventually recover their money after involving banks, regulators, or legal channels. The key is refusing to let the issue quietly disappear.

How To Protect Yourself Next Time

Always cancel insurance policies in writing and save confirmation emails permanently. Disable autopay separately if possible. Monitor your bank account closely for at least two billing cycles after cancellation. Using a credit card instead of direct bank withdrawals can also provide stronger consumer protections. A little preparation can prevent a major financial headache later.

Final Thoughts On Fighting Unauthorized Charges

Nobody expects canceling car insurance to become a months-long battle. Yet billing errors and poor customer service remain common frustrations in the insurance industry. Knowing your rights and acting quickly can dramatically improve your chances of getting your money back. Stay organized, stay calm, and document everything. Consumers have more leverage than they often realize.

You May Also Like:

My car was towed, when as far as I can tell I was parked legally. Can that really happen?