The Sticker Shock After Moving States

You moved to Texas expecting some changes, but your car insurance premium doubled. It felt like a punch to the gut. You wonder if it’s some kind of mistake or unfair pricing practices. The reality is that insurance rates can vary by a lot from one state to another, and your new location alone can significantly impact what you pay.

Yes, This Is Absolutely Possible

Car insurance rates in the United States vary widely depending on where you live. Just moving across state lines can cause major price changes, even if you have a clean driving record and your vehicle stays exactly the same. In some cases, drivers see jumps of hundreds or even thousands of dollars annually.

Idaho Is One Of The Cheapest States

Idaho consistently ranks among the cheapest states for car insurance. Its low population density, lighter traffic, and fewer accidents all help keep premiums down. Drivers in Idaho often pay a lot less than the national average, which sets a low baseline before any move.

User:akampfer, Wikimedia Commons

User:akampfer, Wikimedia Commons

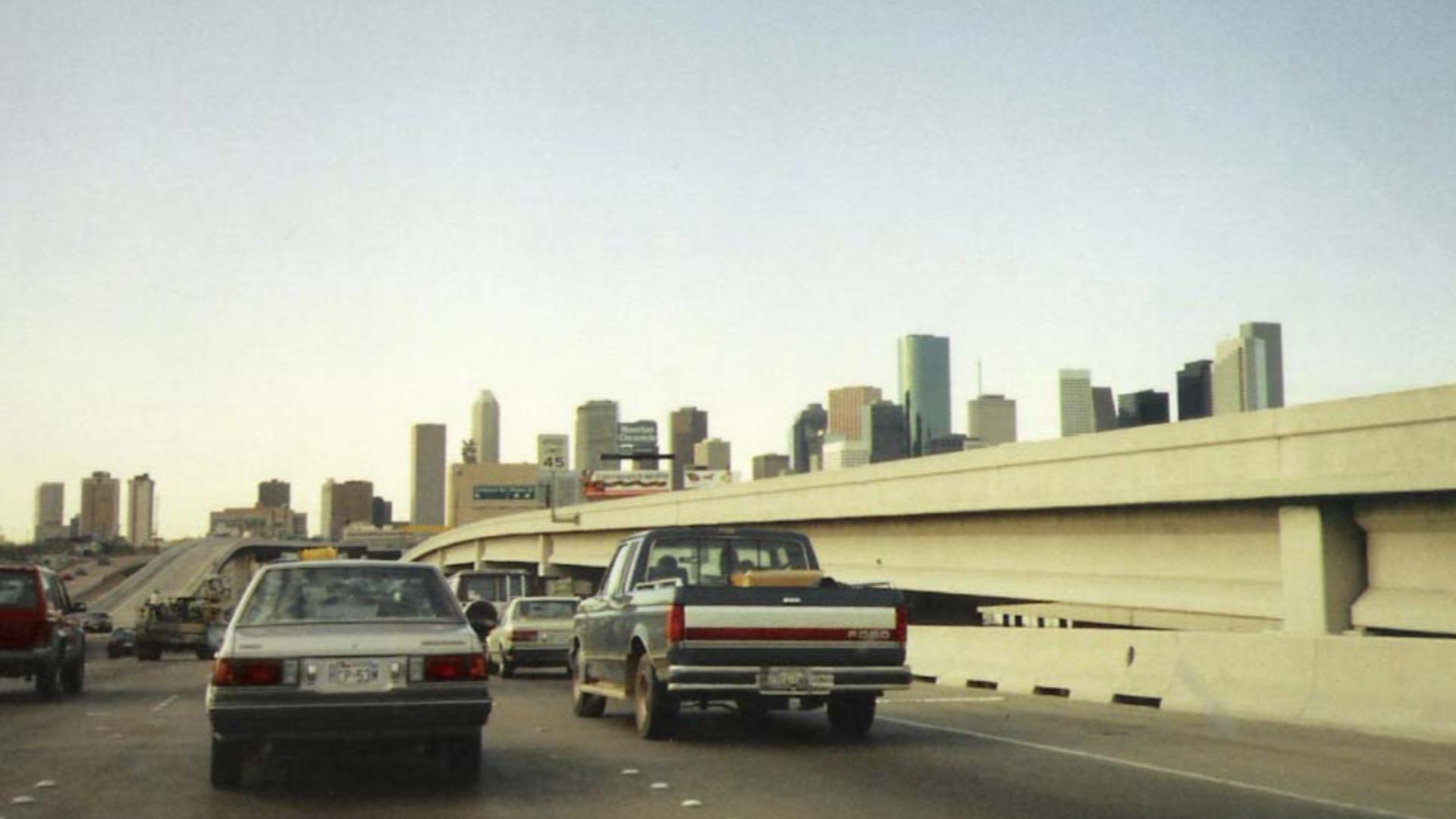

Texas Can Be Much More Expensive

Texas sits on the opposite end of the cost spectrum. Average premiums can be around $1,500 dollars per year or more, with wide variation depending on location. Urban areas and higher risks push prices upward even more, making Texas noticeably more expensive than states like Idaho.

Population Density Drives Risk

One big factor is population density. Texas has large metro areas with heavy traffic, while Idaho is more rural. More cars on the road increase the likelihood of accidents, and insurers price that risk directly into your premium.

Hequals2henry, Wikimedia Commons

Hequals2henry, Wikimedia Commons

Urban Living Raises Rates

If you moved to a city like Houston, Dallas, or Austin, your rates likely increased even more. Urban environments bring higher accident rates, more theft, and greater claim frequency, all of which insurers factor into your pricing.

Ansem27 at English Wikipedia, Wikimedia Commons

Ansem27 at English Wikipedia, Wikimedia Commons

Weather And Natural Risks Matter

Texas faces more severe weather risks than Idaho, including hail, flooding, and hurricanes in some regions. These environmental risks also play a role in the likelihood of insurance claims, which in turn raises premiums even more for everyone in the area.

Jacinta Quesada, Wikimedia Commons

Jacinta Quesada, Wikimedia Commons

Repair Costs Are Higher

Insurance companies also take into account how much it costs to repair vehicles. In Texas, higher labor costs, parts prices, and overall cost of living can drive up claim expenses, which brings higher premiums compared to lower-cost states.

State Laws Affect Pricing

Each state sets its own insurance requirements. Texas may require higher minimum coverage or have different liability standards than Idaho, which can increase your base premium even before adding optional coverage.

Tingey Injury Law Firm, Unsplash

Tingey Injury Law Firm, Unsplash

Uninsured Drivers Play A Role

The percentage of uninsured drivers varies by state. In areas where more drivers lack coverage, insurers raise rates on those with insurance in order to offset the increased financial risk of accidents involving uninsured motorists.

Shuets Udono, Wikimedia Commons

Shuets Udono, Wikimedia Commons

Your ZIP Code Matters More Than You Think

Insurance pricing can change dramatically by location even within the same state. Even moving across town can affect your rate. Insurers look at crime rates, accident frequency, and claim history at the ZIP code level when setting premiums.

Quintin Soloviev, Wikimedia Commons

Quintin Soloviev, Wikimedia Commons

Rates Have Been Rising Nationwide

Insurance costs have increased all across the country on average in recent years. Factors like inflation, higher vehicle costs, and more expensive repairs have pushed premiums upward, especially in states like Texas where increases have been particularly steep.

Your Personal Profile Still Matters

Even though location plays a huge role, your personal factors are still important. Your driving history, age, credit score, and vehicle type all affect your premium, and changes in any of these can magnify the increase after a move.

It Isn’t A Mistake

When your rate doubles, it may feel like an error, but it usually isn’t. Insurance pricing models are highly data-driven, and take every last cent into account. That means a move from a low-risk state to a higher-risk one can legitimately cause a dramatic increase.

Shop Around Immediately

One of the best things you can do in the short term is compare quotes from multiple insurers. Rates vary widely between companies, and switching providers can often reduce your premium significantly without sacrificing coverage.

Adjust Your Coverage Thoughtfully

You may be able to lower your premium by adjusting your coverage. Raising your deductible, removing unnecessary add-ons, or reevaluating full coverage versus liability are all moves that can make a meaningful difference in your monthly cost.

Ask About Discounts

Many insurers offer discounts for safe driving, bundling policies, good credit, or installing safety features. These discounts can help you offset the higher base rates you run into after moving to a more expensive state.

Consider Usage-Based Insurance

Some companies offer programs that track your driving habits. If you are a safe driver, these programs can lower your premium by rewarding cautious behavior behind the wheel.

Improve What You Can Control

Maintaining a clean driving record, improving your credit score, and choosing a less expensive vehicle to insure can all help bring down your costs over time. While you can’t change your location, you can influence other pricing factors.

Final Takeaway

Yes, your insurance doubling after moving from Idaho to Texas is absolutely possible. The change reflects higher risk, denser traffic, and different state factors. The good news is that you’re not stuck with that rate. By shopping around and adjusting your policy, you can often bring it back down to something more manageable.

You May Also Like: