The Tiny Box Hidden In Plain Sight

You sign the finance papers, drive home, and assume the deal is finished. Then months later, a mechanic spots a small device under the dash, or you find out your lender may be able to track the car, or even shut it off. It sounds like a paranoid fantasy, but it really happens. In some financed car deals, GPS tracking devices really are installed, and whether that is legal often depends on what you agreed to and what state law says.

Yes, Dealers And Lenders Sometimes Do This

GPS devices and starter interrupt systems have been part of subprime auto lending for years. The Federal Trade Commission has documented how some buy-here, pay-here dealers used technology that could track a vehicle’s location and even disable it. These systems are usually sold as tools for recovering cars after default, but they also raise obvious privacy and disclosure concerns.

Buy Here Pay Here Lots Used The Tech Early

Long before the latest FTC case, the agency looked closely at buy-here, pay-here dealers in a report released in January 2014. The FTC found that many dealers used GPS devices and starter interrupt technology in cars sold to people with poor credit. The report said these dealers often relied on aggressive collection and repossession tactics, which made this technology a key part of the business model.

Starter Interrupts Add Another Layer

Some financed cars do not just have GPS units. They also have starter interrupt devices, which can stop a vehicle from starting after a missed payment. The Consumer Financial Protection Bureau has described these tools as part of the high-risk world of subprime auto finance, where collection pressure can be intense and disclosures are not always clear.

Why This Matters More Than It Sounds

A hidden tracker on a financed car is not just about repossession. Location data can show where you sleep, work, worship, and get medical care. That is why regulators and privacy advocates pay so much attention to these devices, especially when buyers are not clearly told what is installed and what it can do.

Your Contract Is Usually The First Place To Look

Can a dealership actually put a GPS tracker on your financed car? Sometimes yes, if the contract clearly allows it and state law does not ban or limit the practice. Financing papers, retail installment contracts, and separate addendum forms may include consent to vehicle tracking technology or starter interrupt devices. If that language is buried, vague, or missing, the dealer or lender may have a much weaker legal argument.

Disclosure Is The Whole Ballgame

The biggest issue is often not whether tracking technology exists. It is whether the buyer gave informed consent. The FTC has repeatedly stressed that important terms must be disclosed clearly and plainly. If a dealer slipped a tracking device into the deal without clearly telling you, that can trigger state consumer protection problems and possible federal scrutiny.

There Is No Blanket National Rule That Says Always Yes

Many drivers want a simple nationwide answer, but the law is more complicated than that. Federal consumer protection law can punish deceptive disclosures, while state laws may deal with privacy, electronic tracking, repossession, debt collection, or notice requirements. So the same device could be disclosed lawfully in one deal and hidden unlawfully in another.

State Law Can Change The Answer Fast

Some states have specific rules on starter interrupt devices or electronic tracking in financed vehicles. California, for example, has rules for buy-here, pay-here dealers that include notice requirements tied to electronic tracking technology and ignition shutdown systems. If your deal happened in a state with detailed disclosure rules, those local laws matter a lot.

California Became A Key Example

California Vehicle Code section 11713.18 sets rules for buy-here, pay-here dealers that use tracking technology and starter interrupt systems. Among other things, dealers must give written disclosures explaining what the technology does and how it works. That does not mean every tracker is illegal. It means quiet installation is much harder to defend when the law requires upfront notice.

Repossession Is Usually The Business Reason

Dealers and finance companies usually justify GPS tracking as a way to find a car after a borrower defaults. That is the main reason these devices spread through riskier corners of auto lending. The legal trouble starts when a company treats that business convenience as more important than telling the customer exactly what is being installed.

The Device May Not Belong To The Dealer For Long

In many financed deals, the retail installment contract is assigned to a lender or finance company soon after the sale. That means the dealership may have installed the device, but the lender or servicer could benefit from the data or use it during collections. If you are trying to figure out who is responsible, you may need to look at both the dealer and the company collecting your payments.

Privacy Experts Have Been Ringing The Alarm

The National Consumer Law Center has written about GPS tracking and starter interrupt devices in subprime auto loans, warning that these technologies can deepen the power imbalance between borrowers and lenders. Consumer advocates say the problem is especially serious when buyers are under financial stress and may not fully understand the paperwork. A hidden tracker can turn an already one-sided deal into something much more invasive.

Not Every Tracker Means Someone Is Watching You Live

There is an important nuance here. Some devices transmit real-time location data, while others mainly help with repossession after default or activate only under certain conditions. Even so, if the equipment can collect your location, the company should not be vague about it. The fact that the device is not monitored every second does not erase the need for disclosure.

The FTC Put The Practice On The Record

In January 2024, the FTC announced a settlement with Passport Automotive Group. The agency said the dealership group failed to clearly disclose key financing terms and, in some cases, told consumers they had to buy costly add-ons. The FTC’s complaint also said Passport installed devices that could collect location data and remotely disable cars without clearly and conspicuously telling buyers.

What The Passport Case Actually Alleged

The FTC said Passport’s dealerships sold “Payment Protection” products that included GPS location technology and kill switches. According to the complaint, those products were sometimes presented in a misleading way during the financing process. The key point for consumers is simple: federal regulators treated the lack of clear disclosure as a real consumer protection problem, not some minor paperwork issue.

Regulators Have Shown They Care About Hidden Add Ons

The Passport case is a strong reminder that regulators are paying attention to undisclosed products and fees in car deals. The FTC’s allegations were not limited to location-capable devices, but those devices were clearly part of the complaint. That matters because it shows hidden tracking tech can fit into a broader pattern of deceptive sales and financing conduct.

The CFPB Has Warned About The Risks

The CFPB’s auto finance examinations and reports have flagged concerns about add-on products, repossession practices, and servicing abuses. While not every warning is specifically about GPS boxes, the agency has made clear that lenders and servicers still have to follow the law when dealing with borrowers, payments, and defaults. In plain English, financing a car does not give a company a free pass to ignore privacy or fairness rules.

What Discovery Usually Looks Like In Real Life

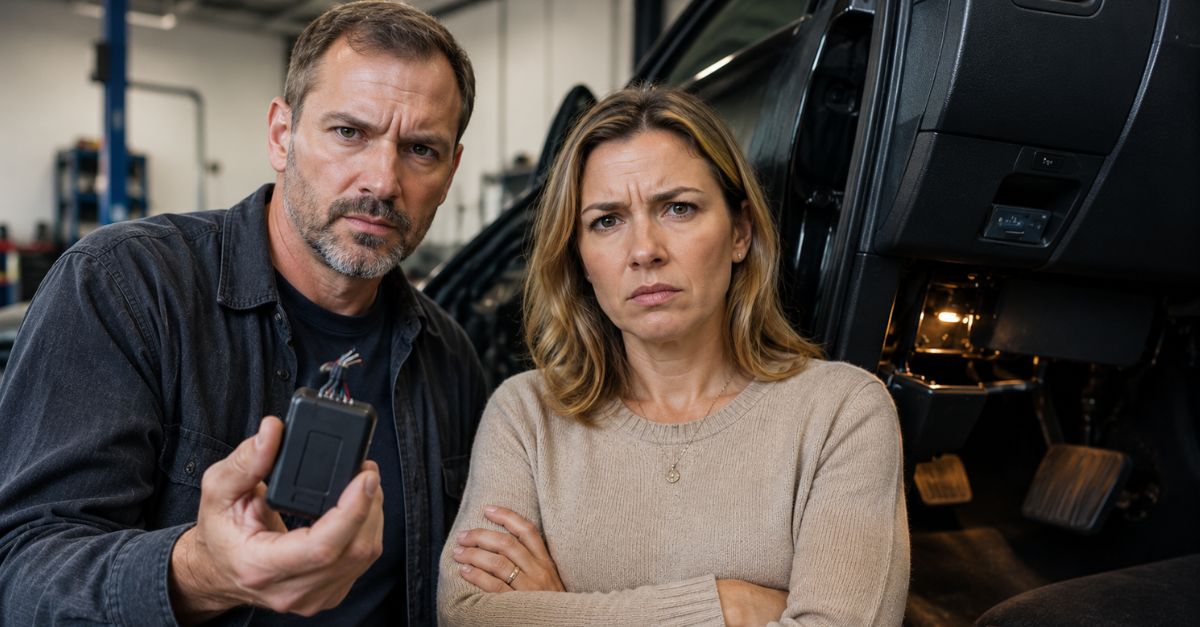

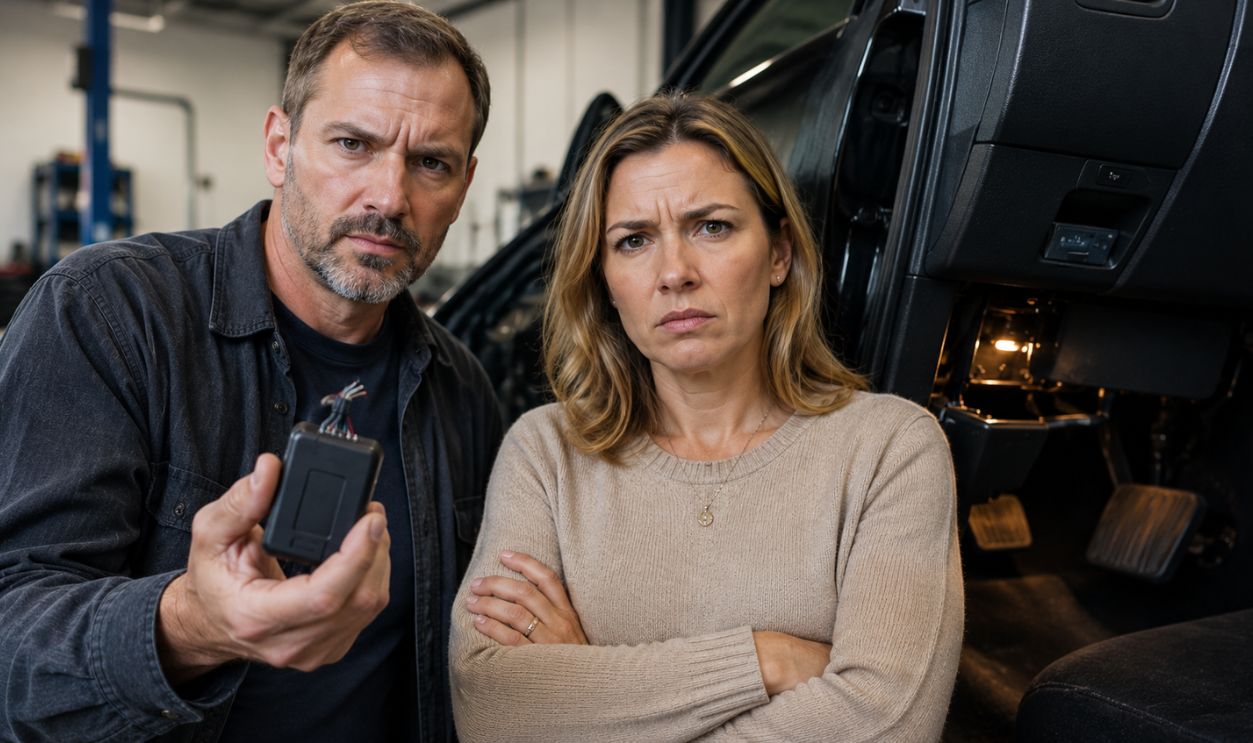

Most drivers do not learn about a tracker because the dealer volunteers the information later. They find out during repairs, after a repossession scare, or when a technician spots a device under the dash or near the OBD-II port. That delayed discovery is exactly why clear written disclosure matters so much at the time of sale.

You May Have A Stronger Case If The Device Was Sold As An Add On

If the tracker was bundled into a paid product, your legal position may be stronger if the fee was hidden or falsely described. The FTC’s complaint against Passport focused on deceptive add-on practices alongside the tracking and disable technology. When a dealer charges you for something invasive and fails to explain it, regulators tend to take that very seriously.

If You Never Clearly Agreed, Start Gathering Paperwork

If you suspect your financed car has a tracker, pull every document from the sale and loan. Look for terms like GPS, telematics, payment assurance device, starter interrupt, ignition disable, payment protection, collateral protection, or repossession aid. Also save texts, emails, and voicemails from the dealership or lender, especially if anyone mentioned shutoff technology or locating the vehicle.

Do Not Rip The Device Out Right Away

It may be tempting to remove the device immediately, but stop before doing that. The equipment may be tied to the financing agreement, and removing it could create a separate dispute with the lender. First document it with photos, note where it was found, and consider asking the dealer or finance company in writing to explain what it is and where you agreed to it.

Ask A Very Specific Question

Do not send a vague complaint saying you are uncomfortable. Ask whether any GPS tracking, telematics, starter interrupt, or remote disable device was installed on the vehicle, when it was installed, what company operates it, and where you authorized it in writing. A direct question can force a direct answer, and written replies can help if the dispute gets bigger.

Servicemembers Have Extra Protections In Some Situations

If you are an active-duty servicemember, separate legal protections may apply in finance and repossession situations under federal law. Those rules do not automatically ban a GPS device, but they can affect what a lender may do if you fall behind. If military status is part of your situation, it is worth getting legal advice geared to that issue.

What You Can Do If The Answer Smells Wrong

If the dealer or lender cannot point to a clear written disclosure, consider filing complaints with your state attorney general, your state consumer protection agency, the FTC, and the CFPB. You can also talk to a consumer law attorney, especially if the tracker was paired with surprise fees, a starter interrupt, or abusive collection tactics. The better your paper trail, the stronger your position.

Can They Actually Do That

The honest answer is yes, sometimes, but not in a free-for-all way. A dealership or lender may be able to install tracking technology on a financed car if the buyer is clearly told and properly agrees, and if state law allows it. If the device was installed without clear disclosure, that is where the company can run into serious legal trouble.

The Bottom Line For Drivers

If you financed a car and later discovered a GPS tracker that was never clearly explained, your concern is justified. This is not some fringe issue, and federal regulators have already challenged dealerships over similar conduct. Read the contract, document everything, ask pointed questions, and do not assume hidden tracking is automatically allowed just because you still owe money on the car.