When “Totaled” Doesn’t Mean Toast

Getting told your car is a total loss is frustrating enough. Finding out the insurance check won't buy you a similar replacement can feel even worse. The good news is that insurance companies can't just make up a number. They have to use specific methods to figure out what your vehicle was worth before the accident.

What “Totaled” Really Means

A lot of people hear the word "totaled" and picture a car that's been crushed beyond recognition. In reality, a vehicle can be declared a total loss even if it still looks repairable. It simply means the insurer believes fixing it would cost more than the car is worth.

Can The Insurance Company Make That Call?

In most cases, yes. Insurance companies are allowed to decide whether a vehicle is a total loss. However, that decision has to be based on repair estimates, vehicle values, and state rules, not just what saves them money.

The Number That Matters Most

When an insurer values your vehicle, they're usually looking at something called Actual Cash Value, or ACV. That's basically what your car was worth right before the accident happened. It's not necessarily what you paid for it or what it would cost to replace it today.

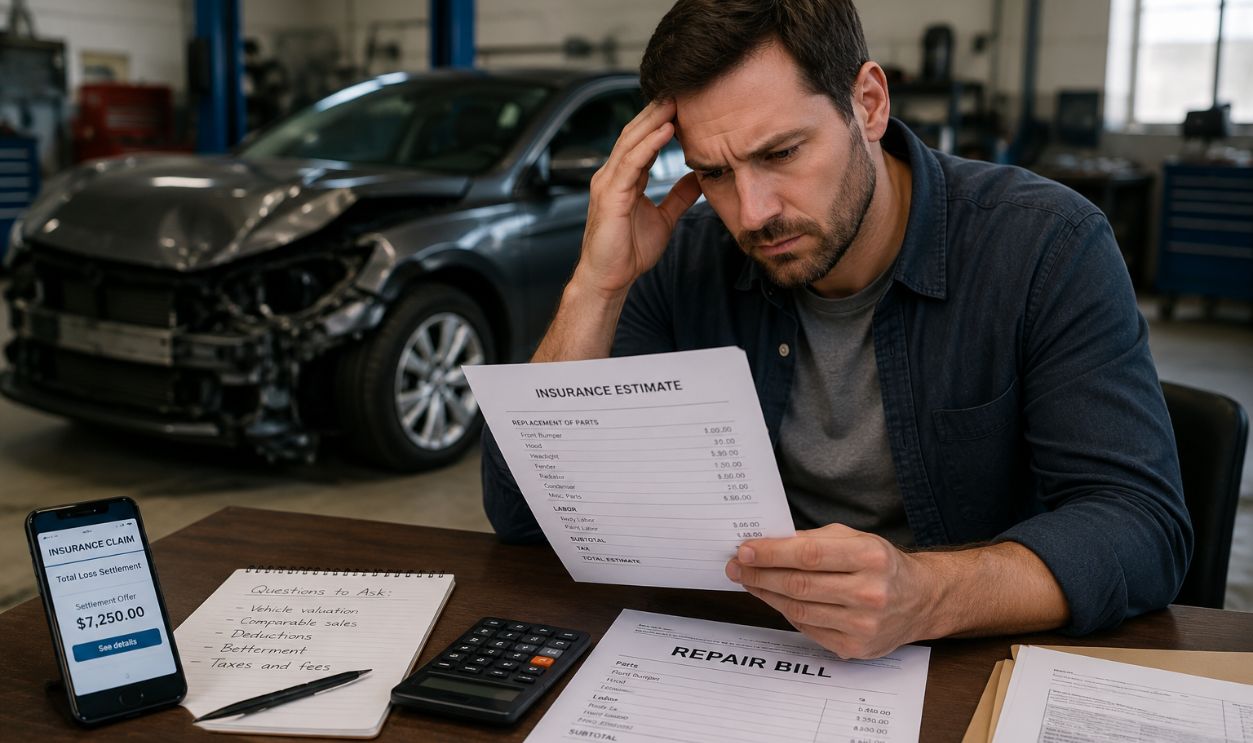

Why The Check Feels So Small

Many drivers start shopping for replacement vehicles and quickly realize they cost more than the settlement offer. That's because insurance companies generally pay based on market value after depreciation, not the cost of buying another car from a dealership.

Depreciation Never Takes A Day Off

Cars lose value every year, even when they're well maintained. Your vehicle may have been running perfectly and still worth less on paper than you expected. Unfortunately, depreciation is one of the biggest reasons total-loss settlements feel disappointing.

State Rules Can Change Things

Different states have different standards for deciding when a vehicle becomes a total loss. In some places, if repair costs reach a certain percentage of the vehicle's value, the insurer may be required to declare it totaled.

The Formula Behind The Decision

Many insurers use a simple calculation. They compare repair costs and salvage value against the vehicle's pre-accident value. If the numbers don't make financial sense, the vehicle gets classified as a total loss.

How They Figure Out What Your Car Was Worth

Insurance companies typically use vehicle valuation services that compare your car to similar ones sold in your area. Things like mileage, trim level, options, and overall condition all play a role in the final number.

Mileage Can Move The Needle

Two identical cars can have very different values if one has significantly more miles than the other. High mileage often lowers the settlement, while unusually low mileage can sometimes help boost it.

Those Extra Features Matter

Leather seats, upgraded wheels, premium sound systems, and advanced safety packages can all add value. If the insurer missed any factory-installed options, your valuation could be lower than it should be.

Keep Those Service Records

Maintenance records won't magically erase depreciation, but they can help prove your vehicle was in excellent condition. That can become useful if you're challenging the insurer's estimate.

The First Offer Isn't Always The Final Offer

A lot of people assume they have to accept whatever number appears on the first settlement letter. That's not necessarily true. If you think the valuation is wrong, you can push back and ask for a review.

Ask To See Their Homework

One of the smartest things you can do is request the valuation report. Sometimes you'll find mistakes such as incorrect mileage, missing features, or comparisons to vehicles that aren't really similar to yours.

Do Some Comparison Shopping

If cars like yours are selling for more than the insurance company says it's worth, gather evidence. Listings from local dealers and private sellers can strengthen your argument during negotiations.

Bringing In An Independent Appraiser

If you're still not getting anywhere, an independent appraisal may help. Having a professional provide a separate valuation can give you additional leverage when discussing the settlement.

What Happens If You Still Have A Loan?

This is where many drivers get an unpleasant surprise. The insurance company only pays what the vehicle was worth, not what you still owe on it. If your loan balance is higher than the settlement, you're responsible for the difference.

GAP Coverage Can Save The Day

That's exactly why GAP insurance exists. It can help cover the gap between the insurance payout and the remaining loan balance, preventing you from paying thousands of dollars out of pocket.

Keeping The Vehicle Is Sometimes Possible

In some situations, you can choose to keep your totaled vehicle. The insurance company will usually reduce your settlement by the car's salvage value, and you may have to deal with special title requirements afterward.

Don't Forget About Taxes And Fees

Depending on where you live, the settlement may include certain taxes, title fees, or registration costs tied to replacing the vehicle. These items are easy to overlook, so it's worth asking about them.

The Bottom Line

Insurance companies can decide that a vehicle is totaled, but they can't do it without a reason. Their decision should be based on repair costs, vehicle value, and state requirements. If the payout seems too low, don't assume you're stuck with it. Review the valuation, look for mistakes, gather evidence, and negotiate. You may end up with a better settlement than the first number they offered.

You May Also Like:

I Bought A Car Two Days Ago And Already Hate It. The Dealer Won't Let Me Exchange It—Is That Legal?