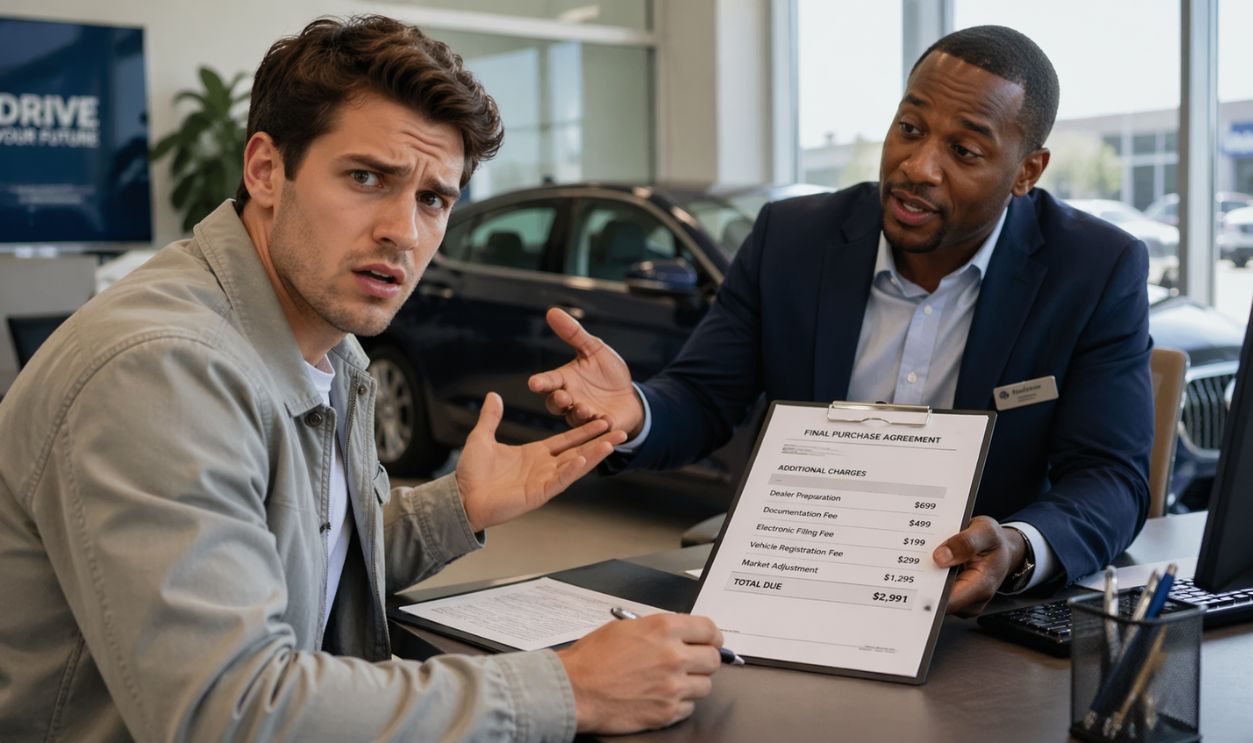

The Sticker Shock That Hits In The Finance Office

Buying a car is a big deal, so when it suddenly gets a lot more expensive when you finally sit down to sign, it's insult to injury. Luckily, in many cases you can still walk away before you sign a binding contract, but it depends on what you've already agreed to.

Why This Happens So Often

Price disputes at dealerships often blow up right at the end, when buyers are tired and ready to be done. The Federal Trade Commission has warned that some dealers advertise one price and then tack on charges later. That issue was a major focus of the FTC’s Cars Rule announced in December 2023. The rule is still being fought in court, but the FTC’s description of junk-fee tactics gives buyers a useful guide.

The Big Question Is Whether You Already Have A Contract

If you have not signed the final purchase contract, you can usually leave. A verbal agreement or handshake is generally not the same as a completed car sale. The key point is whether the final paperwork has been signed and any required conditions have been met.

Signing Day Is Often The Last Real Exit Ramp

For many buyers, the finance and insurance office is the last clean chance to stop the deal. If you see add-ons or fees you do not want, you can say no and get up. That may feel awkward in the moment, but awkward is cheaper than paying for charges you never agreed to.

What Counts As A Surprise Fee

Common examples include nitrogen-filled tires, paint protection, VIN etching, fabric protection, anti-theft products, and document fees that were not clearly disclosed upfront. Some charges are real and common, but that does not mean every fee is required. The real question is whether the charge was disclosed, described honestly, and actually necessary to complete the sale.

SipleDailyUser, Wikimedia Commons

SipleDailyUser, Wikimedia Commons

Not Every Fee Is Fake, But Not Every Fee Is Required

Taxes and state registration charges are usually real and unavoidable. A dealer document fee may also be allowed under state law, though the amount and disclosure rules depend on the state. Add-on products and services, though, are often optional, even when the salesperson acts like they are not.

The FTC Has Warned About Add-Ons Specifically

When the FTC announced the Combating Auto Retail Scams Rule on December 12, 2023, it pointed to bait-and-switch pricing and charges for add-ons that gave no benefit or were not approved by buyers. That matters because federal regulators were talking about these exact last-minute fee problems. Even though the rule’s legal status is still unsettled, the conduct it describes is familiar to plenty of car shoppers.

Harrison Keely, Wikimedia Commons

Harrison Keely, Wikimedia Commons

What The CFPB Found In Dealer Financing

The Consumer Financial Protection Bureau has also warned buyers to look closely at the total cost before signing. Its guidance tells consumers to review the out-the-door price, question fees and extras, and avoid signing until every line makes sense. That advice matters because the final contract, not the sales pitch, is what usually controls.

G. Edward Johnson, Wikimedia Commons

G. Edward Johnson, Wikimedia Commons

If You Have Not Signed, Your Leverage Is Strong

Before signing, your biggest advantage is your ability to walk out. Dealers want to close the deal that day, and that gives you leverage when surprise charges appear. You can demand that the fee be removed, ask for a corrected buyer’s order, or end the deal.

If You Already Signed, The Answer Gets Messier

Once you sign, leaving gets much harder. Despite a common myth, there is usually no automatic three-day cooling-off period for car purchases made at a dealership. The FTC says the cooling-off rule generally applies to sales made at your home, workplace, or temporary seller locations, not regular sales on a dealer lot.

Carol M. Highsmith (born 1946), Wikimedia Commons

Carol M. Highsmith (born 1946), Wikimedia Commons

The Cooling-Off Rule Is Not Your Safety Net Here

This catches a lot of buyers off guard. The FTC’s Cooling-Off Rule gives consumers a short cancellation window for certain door-to-door or off-site sales, but it usually does not cover dealership vehicle purchases. So if you are in the finance office staring at a contract, that is the moment to slow down.

State Law Can Change The Fine Print

Car sales are heavily shaped by state law, which means your exact rights can vary depending on where you buy. Some states regulate document fees, require disclosures for add-ons, or give cancellation rights in limited situations. If a dealer says a fee is mandatory, the safest move is to check with your state attorney general or motor vehicle agency.

California Offers A Good Example Of Specific Rules

California’s Department of Motor Vehicles publishes consumer guidance on dealer fees and contract review. It tells buyers to read the contract carefully and understand every charge before signing. That kind of state guidance drives home the same point: do not assume a late-added item has to stay in the deal.

Coolcaesar at en.wikipedia, Wikimedia Commons

Coolcaesar at en.wikipedia, Wikimedia Commons

Yo-Yo Financing Can Make Things Even More Confusing

Sometimes a buyer signs and takes the car home, only to be told later that financing fell through and new terms are required. Consumer advocates and regulators have warned for years about this spot-delivery, or yo-yo financing, problem. If it happens, your rights depend on the contract language and state law, but it is another reason to read every page before you drive off.

Watch For Preprinted Add-Ons

One of the sneakiest moments comes when optional products are already printed into the worksheet or contract. That can make them look official or unavoidable. If you did not ask for them, ask directly whether they can be removed, and do not settle for vague answers.

Ask For The Out-The-Door Price In Writing

A smart way to avoid signing-day drama is to ask for the full out-the-door price before you ever sit down in finance. That means the vehicle price, dealer fees, taxes, registration, and any add-ons. If the written numbers change later, you have a clear reason to challenge the new charges or leave.

Get Specific About Which Fees Are Government Charges

Dealers sometimes group everything together in a way that makes optional items look official. Ask which amounts go to the state, which go to the lender, and which stay with the dealership. That simple question can quickly separate unavoidable costs from profit-packed extras.

A Good Script Can Save You Money

You do not need to sound like a lawyer. Try this: “I am not signing anything with charges I did not approve. Please remove them or I am leaving.” It is clear, calm, and usually gets everyone focused fast.

Do Not Let Time Pressure Push You Into A Bad Deal

Buyers often hear that the dealership is closing soon, the bank is waiting, or the deal only works tonight. Pressure is part of the sales process, but it does not cancel your right to review the paperwork. If you need more time, take it, even if that means coming back another day.

Bring A Calculator And Use Your Phone

A few minutes of math can reveal a lot. Compare the agreed vehicle price to the final selling price, then compare that to the financed amount and total payments. If any jump does not make sense, stop right there and ask questions until it does.

Optional Products Are Often Cancellable, But Read Carefully

If you already signed and later realize you bought a service contract, GAP coverage, or another add-on you did not want, cancellation may still be possible. Many of these products come with cancellation terms, though refunds may be prorated or handled through the lender. Check the specific product contract right away, because timing matters.

Documentation Matters If Things Go Sideways

Save the ad, price quote, text messages, email exchanges, and every version of the buyer’s order. If a dispute starts later, those records can help show what you were told before signing day. They can also help if you file a complaint with your state attorney general, a consumer protection office, or the FTC.

When A Dealer Says A Fee Is Mandatory

Ask for the legal basis in writing. If the dealer cannot explain why the charge is required by law or lender policy, it may just be an optional profit item. A truly mandatory fee should be easy for the dealership to identify and document.

What To Do If You Feel Trapped In The Office

Stand up, gather your papers, and leave. You do not owe anyone a signature just because they spent time working the deal. Until the contract is finalized, walking out is often your cleanest and cheapest protection.

How Regulators Want You To Shop

The CFPB recommends comparing offers, knowing the total cost, and refusing to sign incomplete or inaccurate forms. The FTC also warns consumers to read the contract and make sure promised terms actually appear in writing. These habits are simple, but they matter because dealership disputes usually come down to what the contract says, not what was said across the desk.

Tony Webster, Wikimedia Commons

Tony Webster, Wikimedia Commons

The Most Honest Answer

If the dealership added fees you first saw on signing day, you can often still walk away if you have not signed the final contract. If you already signed, your options are narrower and depend on the contract, any cancellation terms for add-ons, and your state’s laws. The best move is simple: do not sign until every fee is explained, accepted, and written exactly as agreed.