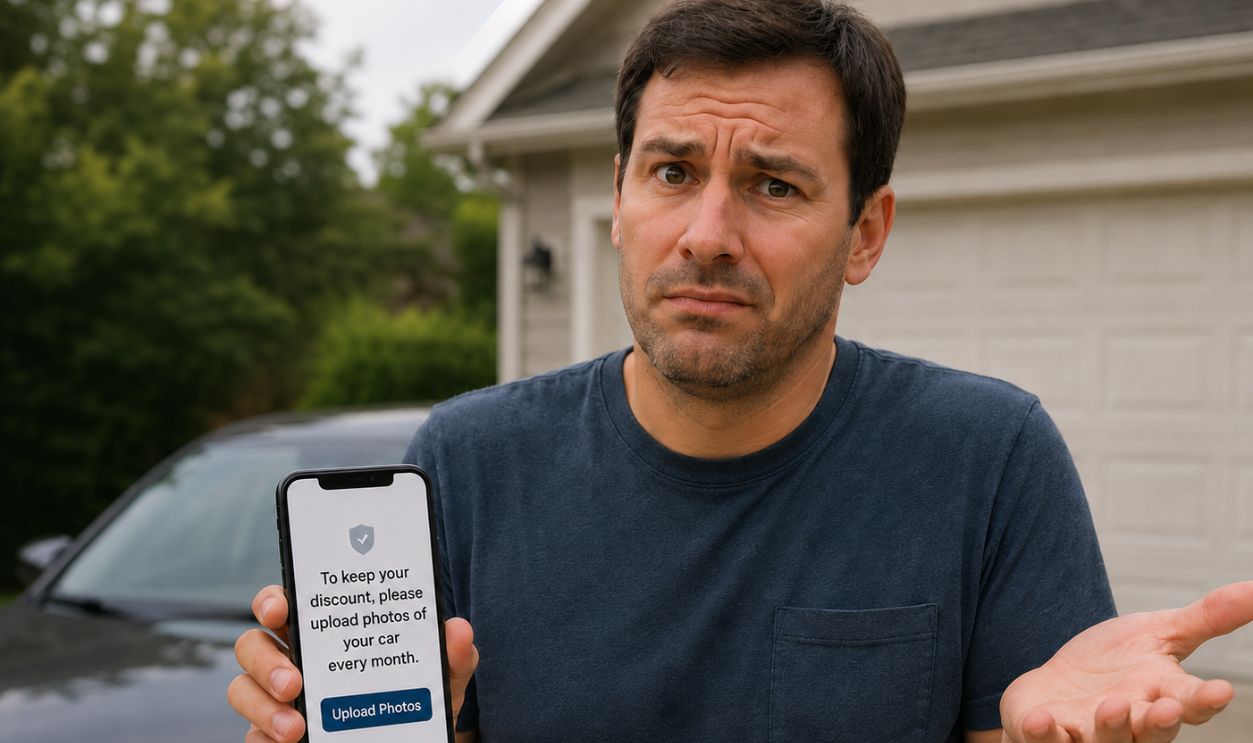

A Strange New Ask From Your Insurer

Programs that reward drivers for documenting mileage or vehicle condition have become more common as insurers look for tighter ways to price risk. It's still not standard everywhere, but it is real enough that major insurers and insurance tech companies now support photo-based verification and app-driven monitoring.

Why This Feels New

For years, the usual insurance discount routine was pretty simple. You bundled policies, kept a clean driving record, or installed a telematics app that tracked braking, speed, and phone use. Asking for recurring photos adds a more hands-on layer, which is why it can feel intrusive even when it is tied to a discount instead of basic coverage.

What Insurers Are Actually Trying To Verify

In most cases, insurers are not asking for monthly photos just to look at your car. They are usually trying to verify one of three things: mileage, garaging location, or vehicle condition. Those checks matter because lower annual mileage and a well-kept car can line up with lower claim risk, and documented proof helps insurers back up how they award discounts.

Mileage Is A Big Reason Photos Show Up

One of the clearest examples comes from pay-per-mile insurance. Metromile, before Lemonade acquired it in 2022, used a device and app-based system built around how many miles a driver actually covered. In California, where mileage-based insurance has gotten special regulatory attention, verified mileage has long been central to usage-based pricing.

California Helped Push Mileage Into The Mainstream

The California Department of Insurance announced in 2019 that it would require insurers to give greater weight to a driver's annual mileage than to ZIP code when setting auto rates. Commissioner Ricardo Lara said the change was meant to reduce pricing practices that hit lower-income drivers and communities of color unfairly. That decision did not order monthly photos, but it did make accurate mileage proof more important.

Low-Mileage Discounts Already Existed Before The Photo Era

Long before photo requests became a talking point, insurers offered discounts for people who drove less. Carriers could ask for odometer readings at renewal or when issuing a policy. The newer twist is using smartphone cameras and apps to verify that information more often and with less manual review.

Photo Inspections Are Not New At All

Here is the part that catches some people off guard. Photo-based insurance inspections have been around for years, especially in underwriting and claims. Companies have increasingly used mobile tools to let drivers submit images instead of scheduling an in-person inspection, and insurance tech vendors have openly sold that as a faster and cheaper option.

Insurtech Companies Built The Tools First

CCC Intelligent Solutions, a major claims and insurance technology company, has promoted photo-based estimating and vehicle image capture tools for years. Snapsheet has done the same with virtual appraisals and claims workflows. Those platforms helped normalize the idea that a phone camera can stand in for an adjuster visit, and that made recurring photo requests much easier for insurers to roll out.

Claims Photos Opened The Door

At first, the pitch was mostly about accidents. Take pictures, upload them, and get an estimate faster. Once insurers and software vendors got comfortable using customer-submitted images in claims, it was a short jump to using similar tools in underwriting, policy verification, and discount checks.

Monthly Photos Still Are Not The Standard For Everyone

This is the key reality check. Most drivers are still more likely to run into telematics tracking, annual mileage questions, or one-time inspection photos than a rule requiring pictures every single month. If your insurer is asking for monthly submissions, it is best understood as a targeted program feature rather than the new normal for every policyholder in America.

Telematics Is More Common Than Photo Check-Ins

State Farm Drive Safe & Save, Progressive Snapshot, Allstate Drivewise, and similar programs usually rely on an app, a plug-in device, or connected-car data. They typically monitor things like hard braking, acceleration, speed, time of day, and distracted driving signals. Those programs are much more widespread than monthly photo requests, which is why your insurer's ask can feel oddly specific.

What A Monthly Photo Program Might Be Tied To

In practice, recurring car photos are often linked to a niche discount or a verification promise. That could mean proving your odometer reading, confirming the car is still garaged where you said it was, or documenting that a vehicle remains in eligible condition for a program. The exact terms should be spelled out in your policy documents or app disclosures, and that is the first place to look.

Some Programs Want Odometer Proof

Odometer fraud is a real issue, and mileage has direct pricing consequences. A photo that includes the VIN and odometer can help verify the number more reliably than a typed entry. If your discount is based on low annual mileage, your insurer has an obvious reason to want visual proof on a recurring schedule.

Why Insurers Care About Condition

Vehicle condition matters because prior damage, modifications, and neglected repairs can change claim severity and repair costs. Insurers have long used inspections to check for existing damage before offering physical damage coverage or special endorsements. A camera-based program can make those checks cheaper and easier, even if it feels like your insurer is peeking into your driveway more often than before.

The Privacy Tradeoff Is The Real Issue

For many drivers, the biggest concern is not the act of snapping a picture. It is what else the photo reveals, like location metadata, a visible address, or details about where the car is parked. If the request comes through an app, it can also involve permissions and data collection practices that deserve a careful read.

Consumer Reports Flagged A Bigger Pattern

Consumer Reports published a widely cited investigation in 2022 showing that many insurer telematics programs collected more data than some consumers may have expected. The review found that companies could gather information related to phone use and driving behavior, depending on the program and permissions involved. That reporting did not focus specifically on monthly car photos, but it underscored a broader shift toward heavier data collection in exchange for discounts.

Regulators Have Been Watching Usage-Based Insurance

The National Association of Insurance Commissioners has tracked the growth of usage-based insurance and the questions it raises around privacy, transparency, and fairness. State insurance departments generally require policy forms and rating plans to be filed and approved, but the details of a discount program can still vary a lot by insurer and state. That means whether a monthly photo requirement is allowed or common may depend partly on where you live and which program you joined.

WavebreakMediaMicro, Adobe Stock

WavebreakMediaMicro, Adobe Stock

This Is Not Quite The Same As Claims Surveillance

It helps to separate routine policy verification from claims investigations. If you file a claim, insurers may seek photos, repair estimates, and other evidence related to the loss. A monthly photo request is different because it is built into discount eligibility before any crash happens, and that is exactly why it can feel more personal.

Why Insurers Like These Programs

The business logic is simple. Better data can mean more precise pricing, less fraud, and fewer disputes about who qualified for what discount. If a driver agrees to provide evidence regularly, the insurer has a stronger paper trail when it comes time to renew the policy or explain a rate change.

Why Drivers Might Actually Like Them

Not every policyholder hates the idea. If you truly drive very little, keep your car in good shape, and do not want a telematics app tracking every hard brake, a quick monthly photo may feel like the less invasive option. For some people, a camera check can seem better than continuous location or behavior monitoring.

But Monthly Can Be A Hassle Fast

Convenience cuts both ways. Missing a submission deadline, taking blurry images, or failing to capture the required angles could put the discount at risk even if your driving habits never changed. That makes the program less about your car alone and more about whether you are willing to keep up with the chore.

Read The Discount Terms Very Carefully

If your insurer says the photos are required to keep a discount, ask for the exact program rules in writing. You want to know how often photos are due, what needs to appear in them, whether metadata is collected, how long the images are stored, and whether failing to submit affects only the discount or your whole policy. Those details matter much more than the marketing pitch in the app.

Ask What Happens If You Say No

This is one of the smartest questions a driver can ask. In many cases, refusing a monitoring-based or verification-based discount program simply means losing the discount, not losing coverage altogether. Still, some underwriting programs may require certain documentation for specific coverages, so it is worth getting a straight answer before you opt out.

Check Whether There Is An Alternative

You may have options. Some insurers can verify mileage during renewal, accept periodic odometer readings instead of monthly full-vehicle photos, or offer a different discount that does not require the same level of documentation. If the request makes you uncomfortable, it is reasonable to ask for a lower-surveillance path.

Shop Around If The Program Feels Excessive

Insurance pricing is fragmented enough that one carrier's quirky requirement is another carrier's nonissue. If a monthly photo routine feels too invasive or too annoying, compare quotes from insurers that rely on more traditional discounts or standard telematics. You may find similar savings without having to turn your camera into part of your policy paperwork.

So Is It Becoming Normal

The honest answer is yes, in a limited way. Photo-based verification is becoming more normal inside insurance operations, especially because claims, inspections, and mileage verification have all gone digital. But a blanket monthly photo requirement for ordinary drivers is still not the industry default, and it remains more of a program-specific tactic than a universal trend.

The Bottom Line For Drivers

If your insurer wants monthly car photos to preserve a discount, treat it like any other data-for-savings trade. Understand exactly what is being verified, what you are giving up, and whether the savings are worth the effort and privacy cost. In today's insurance market, that kind of request is no longer bizarre, but it is still unusual enough that you should read the fine print before you say yes.