Fast Maneuvers

Buying a vehicle can feel final once you sign paperwork, hand over your trade-in, and drive away. But some buyers later receive a call claiming their financing was never approved. When they return the vehicle, they discover their trade-in has already been sold. If this type of scam happens to you, understanding your rights and reviewing your paperwork carefully can make a major difference.

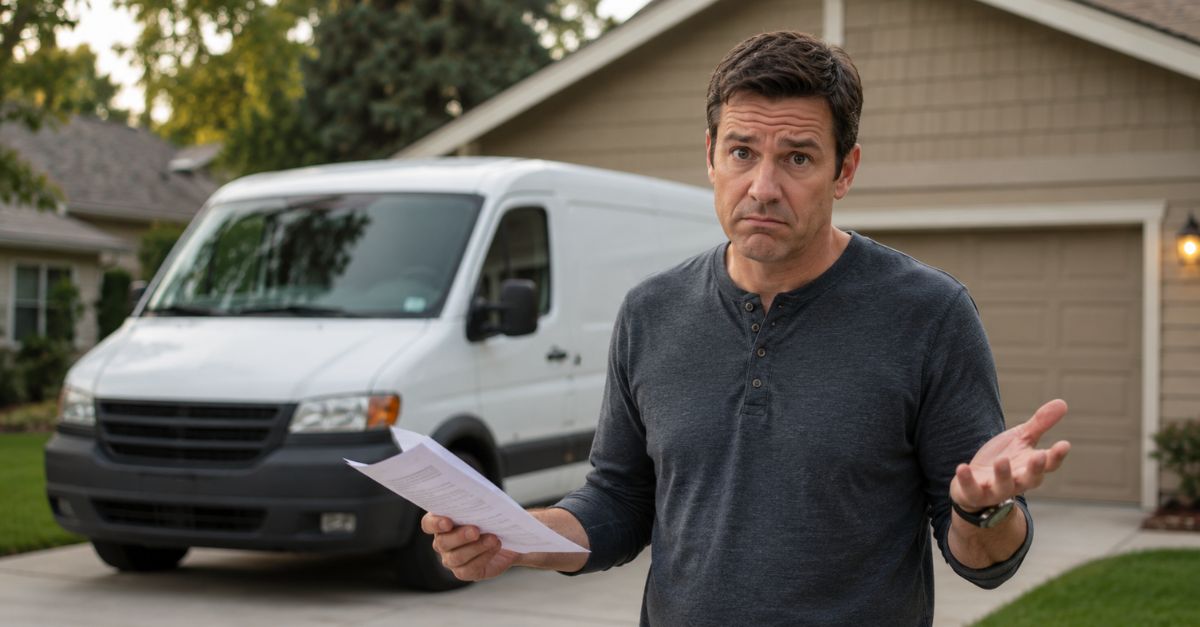

The Call Nobody Expects

You may believe your purchase is complete after signing documents and taking possession of the vehicle. Then the dealership calls days or even weeks later, claiming the financing fell through. Suddenly, you're told to return the car or agree to different financing terms.

Understanding Spot Delivery

Many dealerships use a process called spot delivery. This allows you to take the vehicle home before final financing approval is secured from a lender. The arrangement is legal in many states, but it can create complications if financing is later rejected.

What Yo-Yo Financing Means

Consumer advocates often refer to these situations as "yo-yo financing." You drive away believing the deal is done, only to be called back later and asked to return the vehicle or accept less favorable financing terms.

Check Your Contract

Your first step should be reviewing every document you signed. Some contracts contain language making the sale conditional upon financing approval. The exact wording can significantly affect your legal position and available remedies.

Don't Panic

Receiving a financing rejection call can be stressful, especially if you've already rearranged insurance, registration, and transportation plans. However, avoid making immediate decisions or signing new documents until you understand your rights and obligations.

Vodafone x Rankin everyone.connected, Pexels

Vodafone x Rankin everyone.connected, Pexels

Ask For Documentation

Request written proof that financing was denied. Ask which lender rejected the application, when the decision occurred, and whether other financing options were considered. Having documentation can help you evaluate whether the dealership's explanation is legitimate.

Your Trade-In Matters

The trade-in is often where these disputes become especially complicated. Many buyers assume their old vehicle remains available if financing fails. Unfortunately, dealerships sometimes sell the trade-in before financing is fully resolved.

Discovering It Was Sold

Finding out your trade-in has already been sold can be shocking. You may suddenly be without your old vehicle and unable to keep the new one under the original terms. That situation dramatically changes the stakes of the negotiation.

Do Not Sign Immediately

Some dealerships may present a new contract with higher interest rates, larger down payments, or additional fees. Before signing anything, compare the new terms carefully with the original agreement and consider obtaining independent advice.

State Laws Differ

Your rights depend heavily on where you live. Some states have specific consumer protection laws governing conditional deliveries, financing contingencies, and the treatment of trade-ins when financing is not finalized.

Refund Requirements Vary

Certain states require dealers to return money, deposits, or trade-in value before negotiating a replacement contract. Other states provide different procedures. Understanding your state's rules can be critical when evaluating the dealership's demands.

Demand A Full Accounting

Ask the dealership for a complete written accounting of your transaction. This should include your down payment, trade-in allowance, payoff amounts, taxes, fees, and any proceeds received from selling your trade-in vehicle.

Keep Every Record

Save purchase agreements, financing paperwork, emails, text messages, voicemails, and notes from phone calls. Detailed records can become valuable evidence if the dispute escalates or if legal assistance becomes necessary.

Watch For Pressure Tactics

High-pressure tactics are common in some disputed financing situations. You may be told that you have only hours to act or that you have no choice but to sign new paperwork. Take time to verify those claims independently.

Consider Outside Financing

If you still want the vehicle, obtaining financing through a bank or credit union may provide alternatives. Independent financing can sometimes reduce your dependence on dealership-arranged financing and clarify your available options.

File Consumer Complaints

If you believe the dealership engaged in deceptive practices, consider filing complaints with your state's attorney general, consumer protection office, or motor vehicle regulatory agency. These agencies often investigate recurring patterns of misconduct.

Consult A Lawyer

When substantial money is involved, a consumer protection attorney may be worthwhile. An attorney can review your documents, explain applicable state laws, and determine whether the dealership complied with its legal obligations.

Trade-In Value Disputes

If the dealership cannot return your trade-in because it has already been sold, disputes may arise over its value. Documentation regarding the vehicle's condition, mileage, and market value can become especially important.

Beware Future Deals

If a dealer asks you to take a vehicle home before financing is fully approved, ask detailed questions. Understanding whether the sale is conditional can help prevent unpleasant surprises later.

Read Every Page

Many financing disputes trace back to contract provisions buyers never realized they signed. Taking time to read every page and request copies of all documents can help you identify potential risks before leaving the lot.

Knowledge Is Leverage

The strongest position comes from understanding your paperwork, documenting every interaction, and knowing your state's laws. If your trade-in has already been sold, you may still have important rights, but acting quickly and carefully is essential.

You May Also Like:

The Best New Cars You Can Buy For Under $30,000

Car Dealership Tactics That Customers Should Always Question