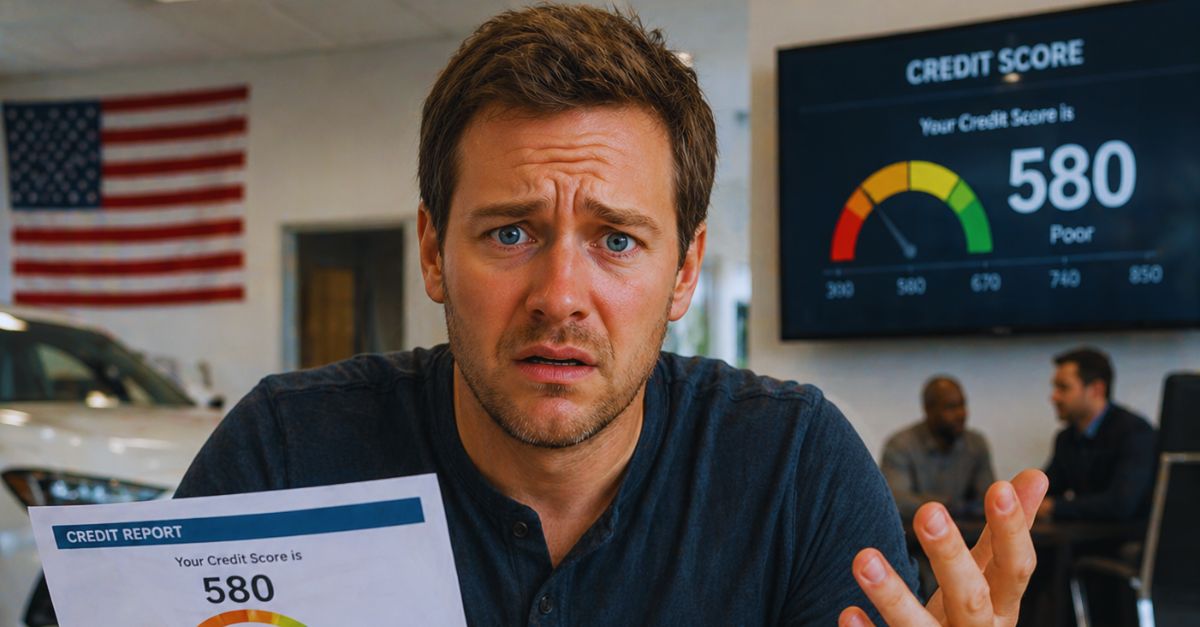

The Surprise In The F&I Office

You sit down to talk numbers, hand over your ID when they ask, and later notice several credit inquiries on your report. It makes sense to be frustrated, because many shoppers will be having the same thought: Did the dealership knock down your credit score several times without asking? Well, to be honest, they might have.

Short Answer First

Maybe, but usually not as badly as people think. Multiple hard inquiries from auto loan shopping are often treated as a single inquiry for scoring if they happen within a set rate-shopping window. That protection exists in major FICO and VantageScore models, though the exact window depends on the model.

Why Dealers Run Credit More Than Once

A dealership may send your application to several lenders to find an approval or a better rate. This is often called shopping your loan. It can lead to multiple hard inquiries on your credit report even if you filled out only one credit application.

What Counts As A Hard Inquiry

A hard inquiry happens when a lender checks your credit to make a lending decision. The Consumer Financial Protection Bureau says hard inquiries can affect your scores, while soft inquiries usually do not. Soft pulls include things like checking your own credit or some prequalification offers.

The Score-Damage Fear Is Real But Often Overstated

FICO says one additional credit inquiry usually takes fewer than five points off a score. It also says rate shopping for an auto loan within a focused period should count as one inquiry for scoring. So the ugly cluster on your report may look worse than it really is.

The Crucial Detail Is The Time Window

This is where the dates matter. FICO says older versions of its scores treat multiple auto loan inquiries made within 14 days as one inquiry. Newer FICO score versions treat them as one when they happen within 45 days.

VantageScore Uses A Different Window

VantageScore says hard inquiries for auto loans made within 14 days are generally counted as one inquiry. That means shoppers can compare offers without getting hit again and again in that model. If your credit service uses VantageScore, that is likely the rule you are seeing.

Why Your Report Can Still Look Messy

Credit scoring and credit reporting are not the same thing. The inquiries can still show up separately on your credit report even if the score treats them as one event. That is why people panic when they see four or five inquiries, even though the score impact may be limited.

Did The Dealer Need Your Permission

In general, a business must have a permissible purpose to get your credit report under the Fair Credit Reporting Act. Applying for financing usually counts. If you signed a credit application or related consent form, the dealer likely had legal cover to send your information to lenders.

But What If You Never Agreed

If a dealer really ran your credit without your authorization and without a valid permissible purpose, that is a different issue. The Federal Trade Commission says the FCRA limits who can access your credit report and why. At that point, the problem is not just a few points on a score. It is whether your rights were violated.

Where Shoppers Get Tripped Up

Many buyers think they only agreed to talk payments or see numbers. Then the salesperson hands over a form that includes broad financing consent in the fine print. If you signed something during the visit, the dealership may argue that you approved the credit pull and any lender submissions that followed.

Spot Delivery Adds More Confusion

Some buyers drive home thinking the deal is done, only to find out financing was still being worked out. In those cases, dealers may keep trying lenders after the first visit. That can cause fresh inquiries days later. They still may fall inside the scoring window, but they can feel like a nasty surprise.

How To Tell Whether It Hurt Your Score

Start by checking the dates of the inquiries and whether they were all for auto lending. Then find out which scoring model your credit monitoring service uses. If the pulls were clustered within 14 or 45 days, depending on the model, the score impact was likely grouped together.

Why Your Score Might Still Drop Anyway

Even when rate-shopping inquiries are grouped, your score can still move for other reasons tied to the same car deal. Opening a new auto loan changes the average age of your accounts, adds new debt, and can change your credit mix. Those factors can affect your score more than the inquiries themselves.

The CFPB’s Practical Warning

The CFPB advises consumers to shop for auto financing within a short period to limit the effect of hard inquiries. That lines up with how major scoring models treat rate shopping. In plain terms, do your loan shopping in days, not weeks.

If The Inquiries Were Spread Out

If the dealership or its lenders pulled your credit over a longer stretch, the grouping protection may not help as much. Separate hard inquiries outside the shopping window can have separate score effects. That is one reason to watch your reports after a messy car-buying process.

What To Do Right Away

Pull your reports from AnnualCreditReport.com and list each inquiry, the date, and the company name. Then gather the paperwork you signed at the dealership, especially the credit application and privacy notices. Those papers can help answer whether the dealer had authorization and when.

Christian Velitchkov, Unsplash

Christian Velitchkov, Unsplash

Ask The Dealer A Direct Question

Call or email the finance manager and ask which lenders received your application and on what dates. Keep it short and specific. You want a written explanation, not a vague line about how this is normal.

When A Dispute Makes Sense

If you see an inquiry from a company you never dealt with, or one that happened after you clearly pulled back your application, dispute it. You can file disputes with the credit bureaus and ask the creditor to prove the permissible purpose. The CFPB also takes complaints when companies fail to fix credit reporting problems.

What The Bureaus Say About Disputes

Equifax, Experian, and TransUnion all let consumers dispute hard inquiries they believe were unauthorized. You usually need identifying information and a clear explanation of why the inquiry is not valid. If the company that reported it cannot verify it, the inquiry may be removed.

Do Unauthorized Inquiries Ruin Credit

Usually not on their own. FICO’s own guidance says one inquiry typically has a small effect for most people. The bigger concern is what unauthorized access says about how your information was handled and whether it could lead to broader fraud or unwanted accounts.

Freeze Versus Fraud Alert

If the inquiries are truly unexplained, think about a credit freeze or at least a fraud alert while you investigate. A freeze restricts access to your report for new credit. A fraud alert tells lenders to verify your identity more carefully. The FTC explains both tools and when to use them.

How To Prevent This Next Time

Before the dealer takes your information, say clearly that you do not authorize a credit pull until you agree in writing. Ask whether the dealer plans to send your application to multiple lenders and how many. Better yet, show up with a preapproval from a bank or credit union so you control when the hard pull happens.

Use Prequalification Carefully

Some lenders offer prequalification with a soft inquiry, which can help you estimate rates before the real application. That gives you a benchmark before you step onto the lot. It also cuts down the pressure to sign broad financing paperwork just to see where you stand.

A Small Score Dip Can Cost Real Money

Even though the point loss from inquiries is often small, auto lending is sensitive to rate tiers. A lower tier can mean a higher APR over a long loan term. That is why it is worth checking whether the dealership’s pulls stayed within normal shopping rules and within your authorization.

The Bottom Line For Most Buyers

If the dealership sent your application to several auto lenders over a short period, those inquiries probably did not crush your score the way the report makes it seem. If you never gave permission, or the pulls kept coming long after the visit, that is when you should push back. The key is telling the difference between a normal rate-shopping cluster and a truly unauthorized credit check.

What To Remember Before You Worry

Check the dates, the lender types, and the paperwork you signed. Multiple inquiries can look ugly on paper while still counting as one for scoring. Frustrating, yes. Catastrophic, usually no.