The Dream Car Versus The Degree

Who doesn't remember being a teenager? A flashy ride can feel like freedom on four wheels. And your daughter has spent the last five years obsessed with one, specific dream car. But when that money has to compete with college savings, housing, and beyond, the stakes get much bigger than horsepower, paint color, or brand. Being the bad guy here is protecting one of the biggest financial commitments most families will ever make.

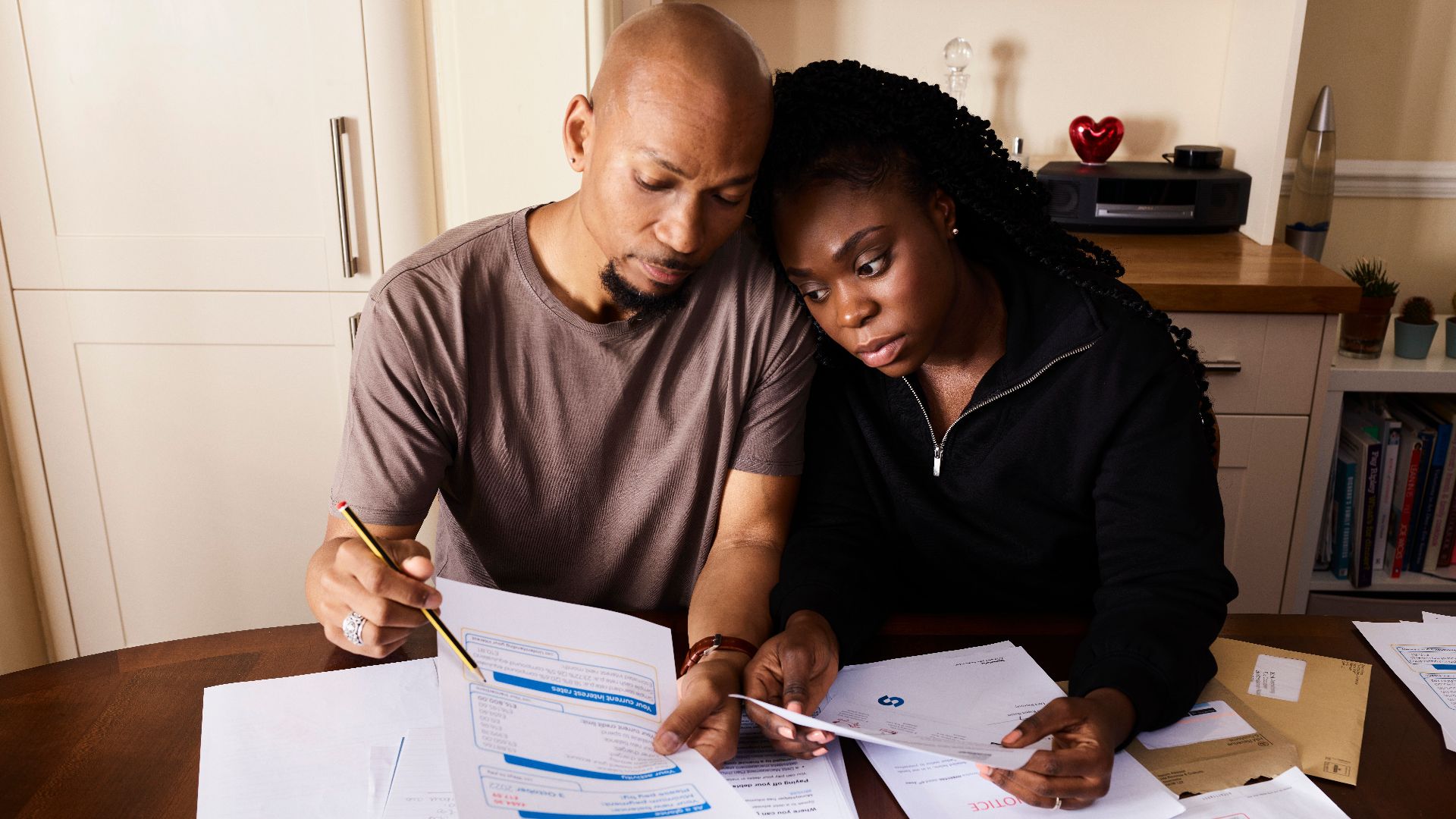

Why This Question Hits So Hard

For many families, college savings represent years of planning, sacrifice, and careful budgeting. A dream car, by contrast, is often an emotional buy with instant payoff and long-term costs. That clash makes this more than a family argument. It is a real financial fork in the road, and the choice can shape the next decade or more.

What College Really Costs Now

The latest published College Board figures show why this decision matters. For the 2024-25 academic year, average published tuition and fees were about $11,610 at in-state public four-year schools, $30,780 at out-of-state public four-year schools, and $43,350 at private nonprofit four-year schools. Once you add housing, food, transportation, books, and other fees, the total cost jumps far past the number many students notice first.

Room And Board Make The Math Brutal

College is not just tuition, and that is where many families get caught off guard. College Board reports that average room and board budgets for 2024-25 reached roughly $13,310 at public four-year schools and $15,250 at private nonprofit four-year schools. Money spent on a car today can easily become money missing from a tuition bill tomorrow.

Student Debt Is Still A Massive Burden

Federal Reserve reporting has kept student debt in the spotlight for a reason. Total student loan debt in the United States still sits in the trillions, and many borrowers carry those balances for years after graduation. Parents who worry about this are not overreacting. They are looking at a debt load that can shape careers, housing choices, and family plans for a long time.

The Used Car Market Is Not Exactly Gentle

If a daughter thinks a dream car is a smart compromise because it is used instead of new, the market still calls for a reality check. Kelley Blue Book has reported elevated used vehicle prices in recent years, even as conditions started to cool from pandemic-era highs. That means a college fund can disappear fast on a vehicle that still comes with age, mileage, and repair risk.

Insurance Can Wreck The Budget Fast

The sale price is only the beginning. AAA notes that insurance is one of the major costs of owning a car, and younger drivers often pay some of the highest premiums because they are considered riskier to insure. A sporty coupe or luxury badge can make that number climb even faster.

Ownership Costs Never Stop At The Sale Price

AAA’s Your Driving Costs study is useful because it shows how cars keep draining money long after the papers are signed. Fuel, maintenance, tires, registration, depreciation, and finance charges all add up. Even a car that looks affordable at first can turn into a steady monthly leak once real ownership begins.

Depreciation Is The Quiet Budget Killer

A college education can build future earning power. A car, even one someone loves, almost always loses value over time. AAA has repeatedly identified depreciation as one of the biggest annual ownership costs, which is a sharp reminder that dream cars are rarely smart long-term assets.

Parents Should First Ask One Crucial Question

Before stepping in, parents should figure out whether the money is legally and practically the student’s to control. If the savings are in a 529 plan, the money is meant for qualified education expenses, and using it for a car purchase generally does not fit that purpose. If the funds are in a regular custodial or joint account, the conversation changes, but the need for guidance does not disappear.

Why The 529 Plan Rules Matter

The IRS is clear that 529 plans come with tax benefits when the money is used for qualified education expenses. If funds are withdrawn for non-qualified purposes, the earnings portion can be subject to income tax and a 10 percent federal penalty, with some exceptions. In plain terms, using college money for a car can create a nasty tax hit on top of an already shaky financial decision.

A Car Purchase Can Also Affect Aid Planning

How families hold and spend education money can affect the bigger college funding picture. Federal Student Aid guidance makes clear that assets and financial resources matter in the aid process, even though treatment depends on the type of account and who owns it. Burning through savings on a vehicle can leave a student more exposed when tuition bills show up than she may realize now.

Yes, Parents Should Sometimes Step In

There are moments when parental intervention is not controlling. It is responsible. If the purchase would put tuition at risk, lead to tax penalties, trigger debt, or lock a young adult into high ongoing costs, stepping in is less about blocking a car and more about protecting financial stability.

But How You Step In Matters

A hard no may stop the sale, but it can also turn the whole thing into a power struggle. A better move is to lay out the full cost with real numbers, including tuition, fees, insurance quotes, maintenance estimates, and what the car will likely be worth a few years from now. Once the math is on the table, the argument often gets a lot less emotional.

Vodafone x Rankin everyone.connected, Pexels

Vodafone x Rankin everyone.connected, Pexels

Turn The Dream Into A Real Budget

Ask your daughter to price the exact vehicle she wants, then build the annual ownership cost line by line. Include insurance, gas, routine maintenance, parking, registration, possible repairs, and realistic depreciation. If she cannot carry those numbers on part-time income or expected post-college earnings, the dream may be outrunning reality.

Insurance Quotes Are A Reality Check

This is one of the easiest and most useful things parents can do. Get real insurance quotes before anyone buys anything, because age, ZIP code, driving record, and vehicle type can all swing the monthly cost. A car that looked barely doable on paper can suddenly look absurd once the premium shows up.

Maintenance Favors Boring Cars For A Reason

Dream cars often come with premium tires, expensive brakes, higher fuel requirements, and pricier parts. Reliable mainstream models may not turn heads, but they usually make life much easier for students with limited income and unpredictable schedules. Practical may not be thrilling, but it helps keep people in class and out of the repair shop.

The Emotional Pull Is Real

Parents should not brush off the emotional side of this. A car can stand for independence, identity, and success, especially for a young adult getting ready to leave home or start a new phase of life. The smartest conversation starts by recognizing that feeling, then bringing in the financial facts without mocking it.

Offer A Middle Ground Instead Of A Brick Wall

If the answer is just no, the discussion can stall out fast. A more useful option is to set a transportation budget that protects education funds while still allowing a reasonable used vehicle, or encourage the student to save separately for the dream model later. That keeps the goal alive without blowing up the near future.

Consider A Safe And Modest Campus Car

For many students, the best answer is not no car. It is the right car. A dependable used sedan, hatchback, or small SUV with good safety ratings and manageable insurance costs can meet transportation needs without burning through a college nest egg.

When A Parent Should Draw A Firm Line

There are clear warning signs that justify a stronger stance. Step in firmly if your daughter would have to empty education savings, take on debt for a fast-depreciating toy, skip important school expenses, or count on you to cover future insurance and repair bills. At that point, the purchase is not just about personal style. It is a real threat to her financial footing.

When Parents Might Reasonably Back Off

If your daughter is an adult, fully understands the costs, has separate non-education funds, can cover ownership expenses herself, and is not expecting a bailout later, the case for parental control gets weaker. Guidance still matters, but so does autonomy. Sometimes the better lesson is letting a young adult live with the outcome of a well-informed decision.

Make The Consequences Explicit

If parents do allow any car purchase tied to family money, the terms should be crystal clear. Spell out who pays for insurance, maintenance, fuel, parking, tickets, deductibles, and surprise repairs. Confusion is where family resentment usually starts.

Put The Agreement In Writing

This may sound formal, but it works. A simple written agreement can define what funds are available, what they can be used for, and what happens if costs go over budget. Families do this not because they do not trust each other, but because memory gets fuzzy once excitement takes over.

Use This As A Money Lesson, Not Just A Car Fight

The bigger opportunity here is financial education. Walk through opportunity cost, taxes, debt, depreciation, and long-term budgeting in a way that connects to a real decision she actually cares about. That lesson will probably outlast both the car and the college years.

The Best Parent Move Is Usually Calm, Not Dramatic

A dream car can heat things up fast, especially if the student feels dismissed and the parents feel panicked. The best intervention is usually a calm, fact-based process that respects the student while protecting the future those savings were meant to support. In moments like this, cool heads can save tens of thousands of dollars.

So, Should Parents Ever Step In?

Yes, especially when college savings are being redirected toward a rapidly depreciating vehicle with ongoing costs the student cannot comfortably carry. The strongest case for stepping in comes when education, taxes, debt risk, or family finances are on the line. The goal is not just to stop the purchase. It is to replace impulse with a smarter plan.